Powell pushes back on March rate cut, BoE on tap

Dollar gains on less-dovish-than-expected Fed

The US dollar gained against all but two of its major counterparts yesterday, losing ground only against the yen and ending the day virtually unchanged against the franc. The main losers were the aussie and the loonie.

What added fuel to the greenback’s engines may have been the less-dovish-than-expected Fed yesterday. The Committee decided to keep interest rates untouched and dropped a longstanding reference to the possibility of further hikes. However, policymakers noted that it may not be appropriate to lower rates until they gain greater confidence that inflation is moving sustainably towards their 2% objective. At the press conference, Fed Chair Powell was more specific, noting that a March rate cut was not the Fed’s “base case.”

This prompted market participants to lower the probability of a rate reduction in March to around 35% from 50% ahead of the decision. Now, a 25bps cut is more than fully priced in for May. That said, the total amount of basis points worth of rate reductions by the end of the year was not affected much. The market still anticipates around 144bps cuts by December, which combined with the fact that there are still participants betting on a March cut suggests that there is room for further upside adjustment to the market’s implied path, and thereby room for further advances in the US dollar.

That upside adjustment and thereby further dollar strength may come on Friday if the US employment report comes in stronger than expected.

Yen stands tall, BoE takes the central bank torch

The dollar could have gained even more after the Fed if it wasn’t for the slide in Treasury yields ahead of the decision, perhaps as investors have already begun reducing their risk exposure by selling stocks and seeking shelter in bonds.

The rush in bonds may have been exacerbated by a 38% selloff in New York Community Bancorp shares after the lender cut its dividends and posted a surprise loss, reviving fears about the health of regional lenders. This allowed the yen to outperform its US counterpart, with dollar/yen briefly falling below 146.00, before rebounding somewhat on Powell’s remarks.

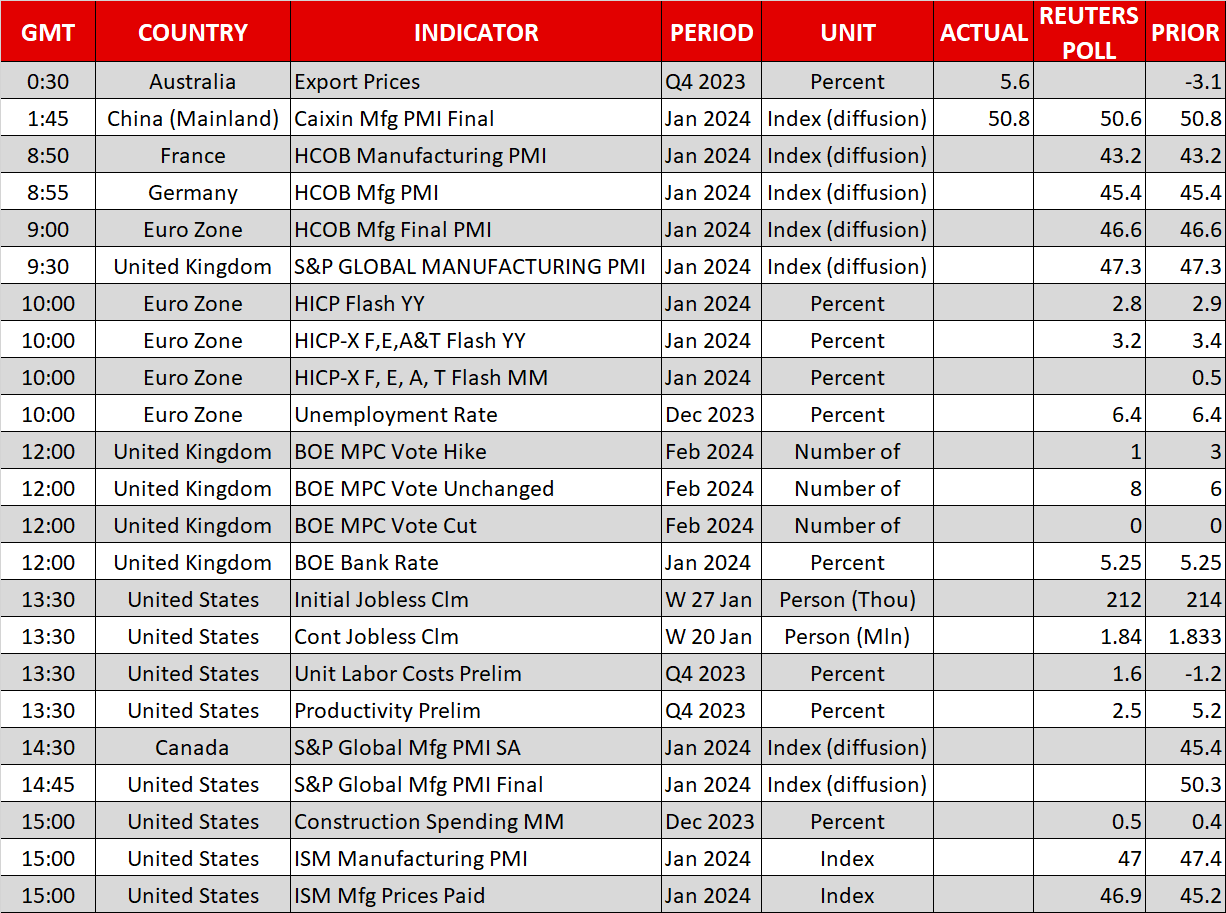

Recent UK data showed that inflation was hotter than expected in December, while the January PMIs pointed to improvement in business activity. Still, investors are penciling in around 107bps worth of rate reductions by the end of the year, with a first quarter-point cut anticipated in June.

As with the market’s implied Fed path, there is room for upside adjustment in the BoE’s path as well should UK officials continue to push back against rate cut speculation, and this might be the case today even if the latest rebound in inflation was the result of base effects. Despite sluggish economic growth in the UK, the improvement in the latest PMIs combined with still-elevated wage growth may allow policymakers to wait for a while longer before shifting to a more dovish stance.

Therefore, should the Bank reiterate the view that it is too early to examine rate reductions, this could help the pound gain some ground, especially if there are once again members opting for a rate increase.

In the Eurozone, the preliminary CPI data for January revealed that the bloc’s inflation slowed by less than expected. However, the euro did not react to the release as traders remained largely convinced that the ECB will deliver its first 25bps cut in April.

Equity traders await more ‘Magnificent 7’ results

On Wall Street, all three of its main indices closed in the red, with the Nasdaq falling more than 2%. Stocks were already falling ahead of the Fed decision, driven by mega-cap tech firms following the disappointing results by Alphabet. The Fed decision served as the icing on the cake. Today, equity investors will digest earnings results by Apple, Amazon and Meta, all of which report after the closing bell.

Gold also pulled back after the Fed poured cold water on March rate cut expectations, but managed to close the day in the green as the early slide in Treasury yields helped the precious metal climb higher in advance.

.jpg "Powell pushes back on March rate cut, BoE on tap")

Stocks perk up but dollar remains heavy as gold extends gains

EBC Markets Briefing | Trade war hammers Aussie; gold sets fresh peak

The crypto market tests the strength of its three-month support

EBC Markets Briefing | A balanced portfolio is more than necessary now

ATFX Market Outlook 16th October 2025

Gold Extends Its Rally as Safe-Haven Demand Builds

Oil Steadies as India Halts Russian Imports, Dollar Weakens on Fed Bets | 16th October 2025