Dollar traders lock gaze on private data

Dollar flexes muscles on hawkish Fed

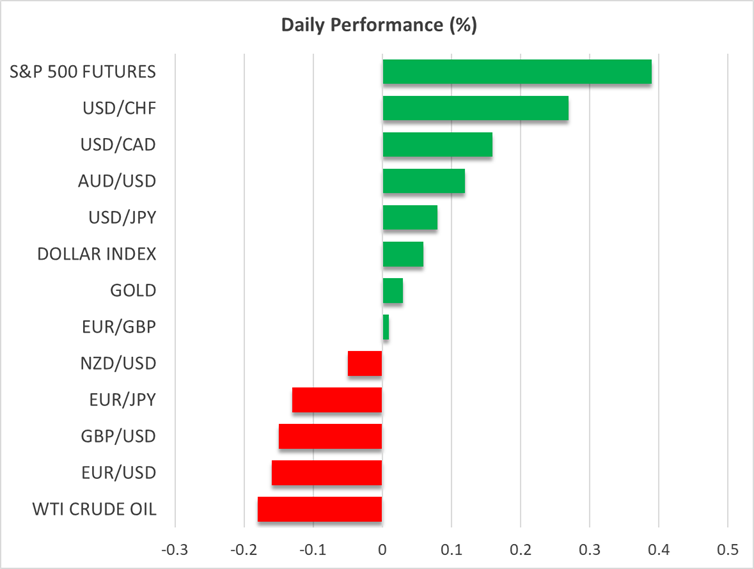

The US dollar continued to gain ground against most of its major counterparts on Friday, but the advance slowed down today as investors are eagerly awaiting the release of private data this week to evaluate how the US economy is faring amid an ongoing US government shutdown and to assess whether the Fed’s hawkish stance last week was appropriate.

On Wednesday, the Fed decided to lower interest rates by 25bps as expected, with Fed Chair Powell pushing back against a December rate cut saying that a further reduction in December “is not a forgone conclusion.” This prompted investors to scale back their rate cut bets, currently pricing in a 68% chance of a quarter-point cut before the turn of the year and 60bps worth of additional reductions for 2026. Ahead of the Fed meeting, a December cut was fully priced in, and another three were penciled in for next year.

ADP and ISM private data to attract extra interest

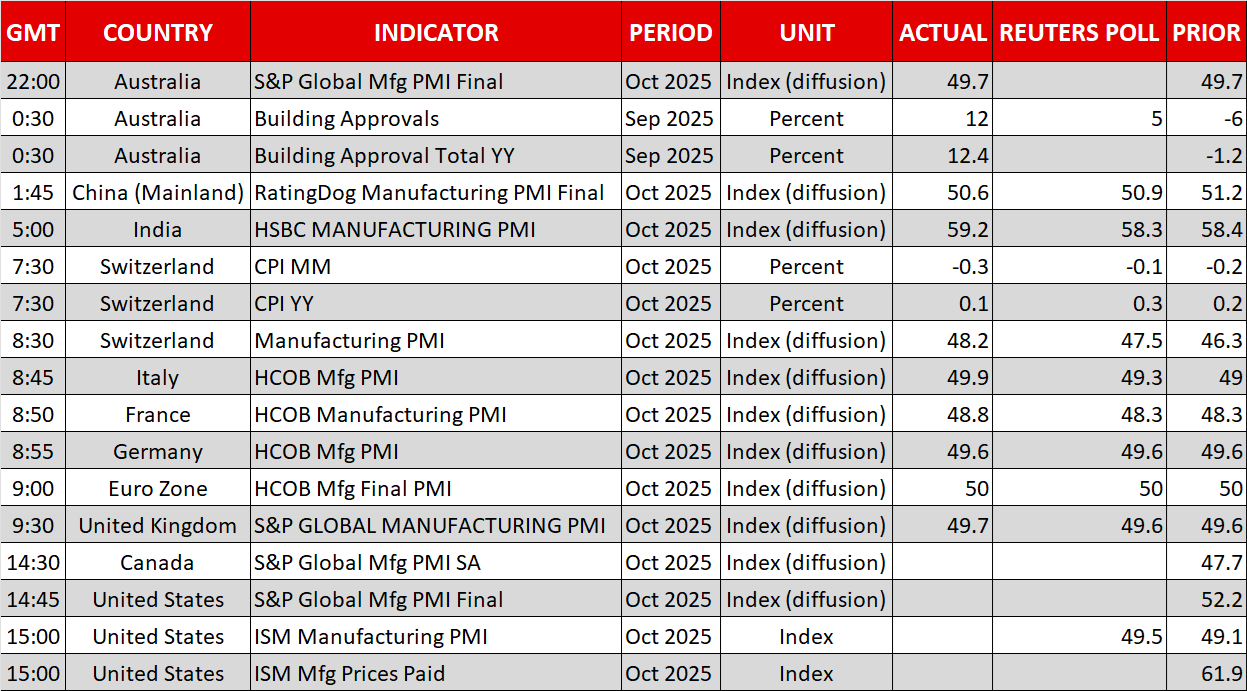

With that in mind, investors may pay extra attention to the ADP employment report on Wednesday – as due to the US government shutdown, no NFP numbers will be released yet – as well as the ISM manufacturing and non-manufacturing PMIs, due out today and on Wednesday, respectively. Should the data suggest that the US economy is faring well despite the shutdown, the US dollar is likely to continue flexing its muscles as investors become even more convinced that the Fed does not have to rush into further rate cuts.

Yen and pound remain wounded

The yen and the pound were the main losers during the month of October, with investors scaling back their BoJ rate hike bets and ramping up speculation about a BoE rate cut before the end of the year.

Although the BoJ reiterated its willingness to raise interest rates, the emphasis on the risks to Japan’s economic recovery did not convince market participants to buy yens, even after Governor Ueda said that the conditions for a rate hike were falling into place and that the chance of the BoJ’s baseline projection to materialize has “heightened somewhat.”

With new PM Takaichi focusing on wage growth and Ueda noting that policymakers want to wait for data to confirm whether salaries will continue rising, investors are fully pricing in a 25bps hike in April, in the midst of the spring wage negotiations.

As for the BoE, it is expected to stand pat on Thursday, but the latest CPI data revealed softer-than-expected inflation for September, while the employment report showed that salaries grew at their slowest pace since 2022 in August and the unemployment rate increased. This gave rise to a 30% probability of a 25bps rate cut this week, with such a move fully priced in by January.

Risk appetite improves further, oil opens with positive gap

On Wall Street, all three of its main indices rebounded on Friday, with US stock futures and Asian indices suggesting that risk appetite entered the new week and month improved. What added fuel to Wall Street’s engines on Friday may have been Amazon’s solid earnings forecasts.

This week, although upbeat ADP and ISM data could add credence to the view that the Fed should not lower borrowing costs aggressively, they could also imply that the US economy is strong enough to withstand a prolonged US government shutdown. Therefore, solid numbers may allow stocks to climb higher. The de-escalation of the US-China trade frictions are also a boost for the broader risk appetite.

Gold rebounded today but remains well below its record high as the improving market sentiment and rising yields are negative variables for the safe haven metal.

Oil prices opened with a positive gap on Monday, after the OPEC+ group decided to pause production hikes for the first three months of 2026. The group raised output by 137k bpd for December, the same as for October and November, but all members agreed that due to seasonality, they will stand pat during the first quarter of next year.

The Trader’s Guide to Gold: Risk Management, Strategy, and Market Awareness

Why Are Oil Prices Falling Even Though the Middle East Conflict Isn't Over?

Margin Debt Is Flashing Red Again

Today Technical Analysis: Gold falls below $4,100 and nears its yearly low as the USD pushes higher

Today Fundamental Analysis: Oil prices drop further as supply fears ease in response to the peace deal

Tech rout and Fed hike bets fuel global risk aversion

PMI Surges to Highest Since 2022; Dollar Index Climbs to One Year High