Israel-Iran conflict remains in focus ahead of Fed decision

New Israel-Iran attacks dent truce hopes

The US dollar slipped against all but one of its major counterparts on Monday, with the Japanese yen posting the largest loss.

With the greenback taking its dusty safe-haven suit out of the closet on Friday amid the military conflict between Israel and Iran, yesterday’s retreat may have been due to hopes that the conflict would ease. According to a Reuters’ report on Monday, Iran asked Qatar, Saudi Arabia and Oman to press US President Trump to talk Israel into agreeing to a ceasefire with Iran, in which case Iran would be willing to return to the negotiating table with the US.

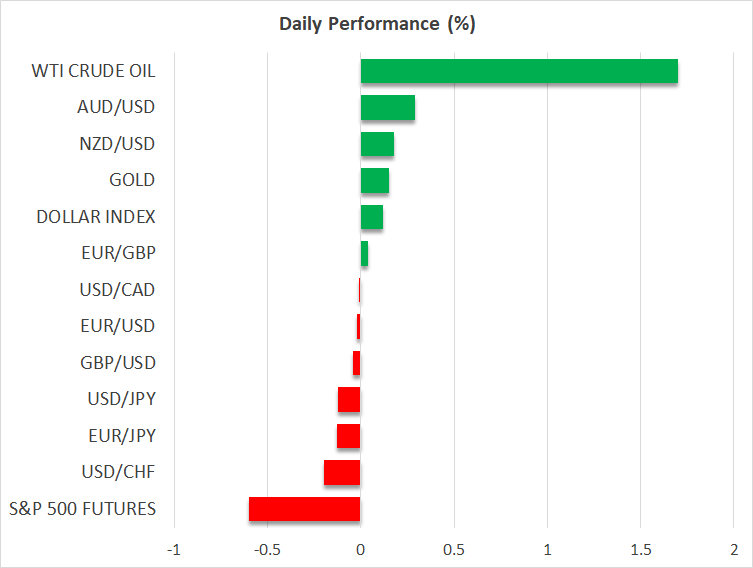

Besides the change in the broader environment, what also contributed to the dollar’s retreat may have been the strong pullback in oil prices on the truce headlines. The retreat in oil means reduced upside risks to inflation and thereby a lower probability of the Fed proceeding with fewer interest rate cuts than previously projected.

Having said all that though, the greenback stabilized today, and oil prices rebounded as concerns re-escalated after US President Trump urged, through his Truth social media platform, the evacuation of Tehran. Today, the conflict enters its fifth day, and the fighting continues with Iranian media reporting new attacks in Tehran and reports emerging that three ships were hit in the Gulf of Oman, near the Strait of Hormuz.

Fed faces tough test amid heightened uncertainty

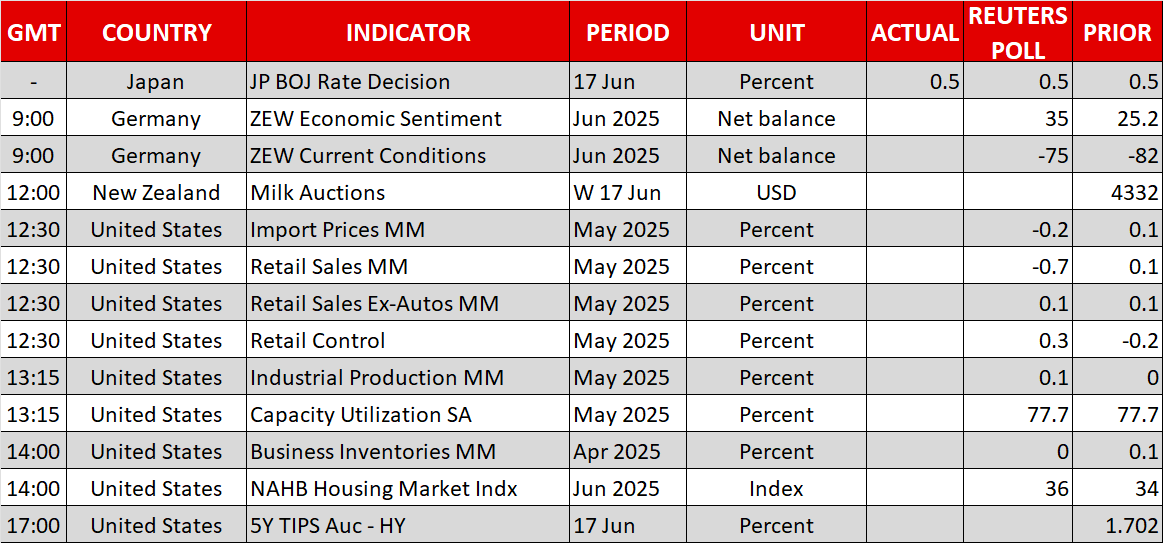

With all this uncertainty clouding the markets, the Fed is due to announce its latest monetary policy decision tomorrow, the outcome of which dollar traders will have to incorporate in their decisions. With inflation in the US remaining sticky and upside risks emerging due to the Israel-Iran conflict, policymakers may need to maintain patience when it comes to interest rate reductions, especially with the Atlanta Fed GDPNow model pointing to a solid 3.8% growth rate for Q2.

According to Fed funds futures, market participants are pencilling in 48bps worth of rate cuts by the turn of the year, more or less agreeing with the Fed’s latest dot plot. A new dot plot will be published on Wednesday, but, despite the upside risks to inflation, the Fed is unlikely to risk signalling only one reduction for this year, as the uncertainty surrounding the economic outlook remains high. That said, a relatively hawkish message could still boost the dollar somewhat.

BoJ remains cautious about future rate hikes

Speaking of central banks, earlier today, the BoJ decided to keep interest rates steady, as was broadly expected, and to decelerate the tapering of its government-purchasing program, noting that they still prefer to move cautiously when it comes to scaling back their decade-long stimulus.

At the press conference following the decision, Governor Ueda reiterated his view that uncertainty about how tariffs could impact the economy remains very high, confirming the notion that they will not rush into hiking interest rates further. Although the yen did not react much, the probability of a rate increase by December was reduced but remained above 50%. Focus now turns to Friday’s National CPI numbers, where more inflation stickiness could allow investors to maintain bets about a hike towards the end of 2025.

Wall Street closes higher, but stock futures slip today

On Wall Street, all three of the major indices closed Monday’s session in the green, with the Nasdaq gaining around 1.5%. The truce headlines may have helped investors increase their risk exposure. However, stock futures are pointing to a lower open today, perhaps due fears of a re-escalation.

Gold was also reactive to geopolitics, pulling back yesterday on reduced safe-haven demand. However, it has yet to regain its shine today, perhaps as the dollar is also turning into a safe haven amid the ongoing conflict between Israel and Iran.

.jpg "Israel-Iran conflict remains in focus ahead of Fed decision")

Oil market prices caught between sanctions and surpluses

Fed, BoC and BoJ meetings enter the limelight

USD/JPY in Correction as Markets Await Signals from Fed and BoJ

EBC Markets Briefing | Gold meanders in the wake of US-China talk

USD/JPY runs out of fuel near July’s high

ATFX Market Outlook 30th July 2025

The 0.6% Surprise: What South Korea’s Growth Means for Your Portfolio