Fragile market appetite ahead of the Fed meeting

Risk sentiment was in retreat on Monday

The week started on a mixed note, as the initial risk-positive market performance during yesterday’s session quickly reversed, with the dollar outperforming across the board - dollar/yen tested the 154.52 level again - and stocks surrendering most of their early gains.

Interestingly, US equity indices exhibited a mixed performance yesterday, with the S&P 500 index registering another all-time high and the more-established Dow Jones recording another negative session. This was the eighth consecutive red day for the Dow, which is the longest streak of negative daily performance since June 2018. A plethora of events back then that included the US-China trade shenanigans, a Fed rate hike and the Iran-US tensions affected risk appetite.

Meanwhile, gold continues to trade sideways today, hovering around the $2,650 level, with bitcoin testing its recent all-time high. Despite the lack of fresh catalysts, the cryptocurrency market remains on fire in anticipation of Trump’s pro-crypto stance. While some analysts are highlighting that the post-election rally has all the ingredients of a price bubble, investors seem confident that cryptocurrencies will remain bid going into the festive period.

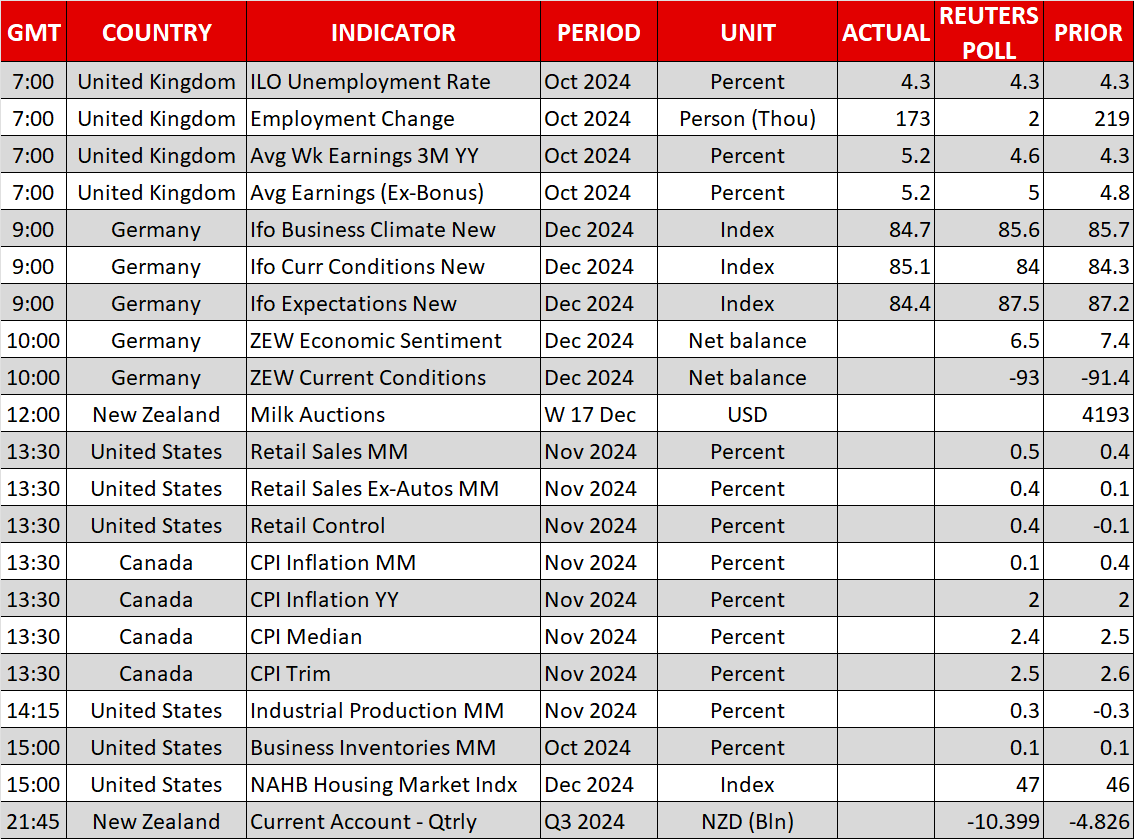

Amidst these developments, the Fed is preparing for a very important meeting on Wednesday. With the usual blackout period limiting Fedspeak, US data does the talking. Following last week's solid CPI report and surprisingly strong PPI data, both the headline retail sales print and the control group indicator are forecast to show a decent improvement today. Despite the strong data figures, the market feels confident that a 25bps rate cut will be announced on Wednesday, predominantly due to Trump’s return to the White House on January 20, 2025.

The chances of a BoE rate cut on Thursday remain very low

The pound started today’s session on a positive note, outperforming both the euro and the dollar, on the back of stronger labour market data. In more detail, the November claimant count change printed well below expectations, while average earnings climbed above the 5% annual growth rate again, bucking the recent trend.

The BoE will hold its final meeting for 2024 on Thursday, and, considering the latest set of data, the 17% probability of a 25bps rate cut currently priced in is probably too optimistic. Pending a very dovish Fed meeting and commentary from Trump about imposing tariffs on the UK as well, the BoE will most likely opt to keep its powder dry for February, when the quarterly report will also be published.

Canada’s Trudeau could be the first victim of Trump’s “America First” agenda

With Germany officially preparing for the February general elections, a political crisis is also brewing in Canada, with Finance Minister and Deputy PM Freeland resigning yesterday, and pressure mounting for PM Trudeau to follow suit. He continues to be deeply unpopular, spelling trouble for his reelection chances in the October 2025 election.

The probability of a snap election has risen exponentially, potentially interfering with the BoC’s willingness to ease further in early 2025. This means that today’s CPI report, which is expected to show a small drop in inflationary pressures, is probably a tad less important in the grand scheme of things. Interestingly, a potential postponement of the BoC’s expected rate cuts in early 2025 might give the loonie some breathing space, especially as the dollar/loonie pair is currently trading at a 4.5-year high.

The yen is about to become a favourite

Dollar trades quietly but headed for worst week since July

Bitcoin stalled at a critical resistance

Bitcoin stalled at a critical resistance

EBC Markets Briefing | Crude prices steady amid thin trading; Nikkei rebounded

GBP/USD Regains Footing, but Underlying Doubts Persist

Will Silver Explode Past $54 or Snap into a Reversal?