Advertisement

Trading Journal

Aug 29, 2018 at 20:03

European indices did not mark today a definite trend. The session was relatively quiet, with no big news, with investors taking advantage of the latest events (last week’s intervention by the President of the Fed and the recent agreement reached between the US and Mexico). Thus, the session was under low volatility and volume below the average observed in August.

Aug 30, 2018 at 23:27

European indices have today been the target of investors’ fears about emerging markets. The situation in Turkey is beginning to show signs of fragility. Yesterday, economic confidence hit the lows since March 2009 (in the midst of the global financial crisis), which led to a further decline in the Turkish Lira against the US Dollar. In the last 3 days, the Turkish currency depreciated by 6% against the US Dollar. Meanwhile in Argentina, Peso lost 8.15% even after President Macri announced that he was negotiating with the IMF on a loan of 50,000 M.USD, which should offset the country’s current inability to fund intentional markets. Since the beginning of the year, Argentino lost 45% of its value against the US Dollar. These two events, although uncorrelated, focused mainly on the securities most exposed to these two economies. In this sense, as Spanish banks BBVA and Santander, as well as Telefónica were particularly targeted by investor sales.

Sep 02, 2018 at 16:24

The delicate phase that crosses Argentina and Turkey has generated turbulence in the exchange markets and by reflex in the financial markets as a whole. This instability has led to an escape of foreign capital from these countries, a move that further pressures their respective currencies.

Sep 03, 2018 at 19:59

The escalation of trade tensions between the US and China influenced the begining of the week, although some European markets managed to close on positive ground in a session that was marked by the closing of the North American market.

Sep 04, 2018 at 20:29

The day was negative for most European markets, in a general context marked by fears about the situation in emerging markets and trade tensions between the US and China. Just like yesterday, automakers were among the worst performers, after over the weekend President Donald Trump said he was prepared to impose additional charges worth 200,000 M.USD on imports from China. Also on the sector weighed the deadlock that is marking the trade talks between the EU and the US, which are centered on the automotive industry.

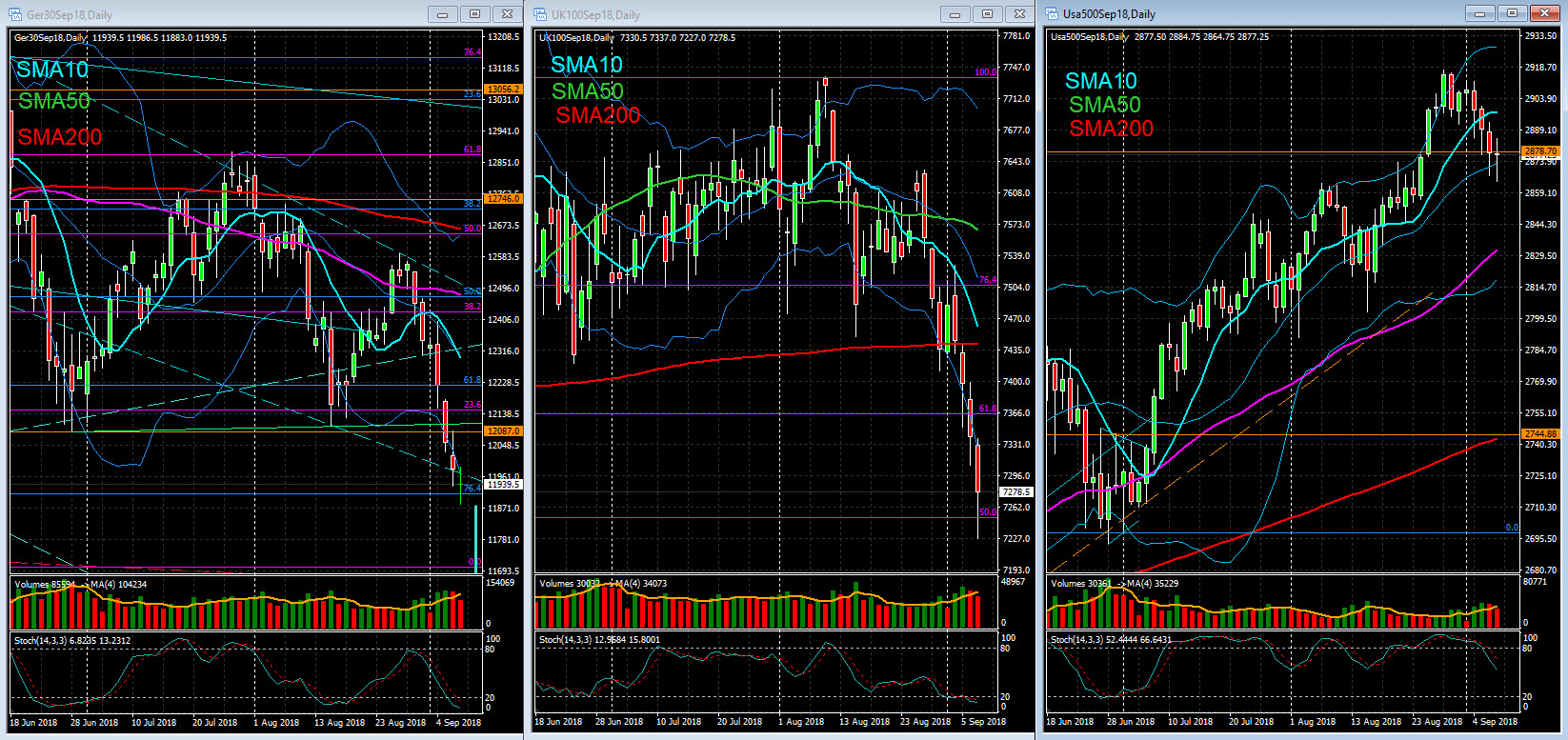

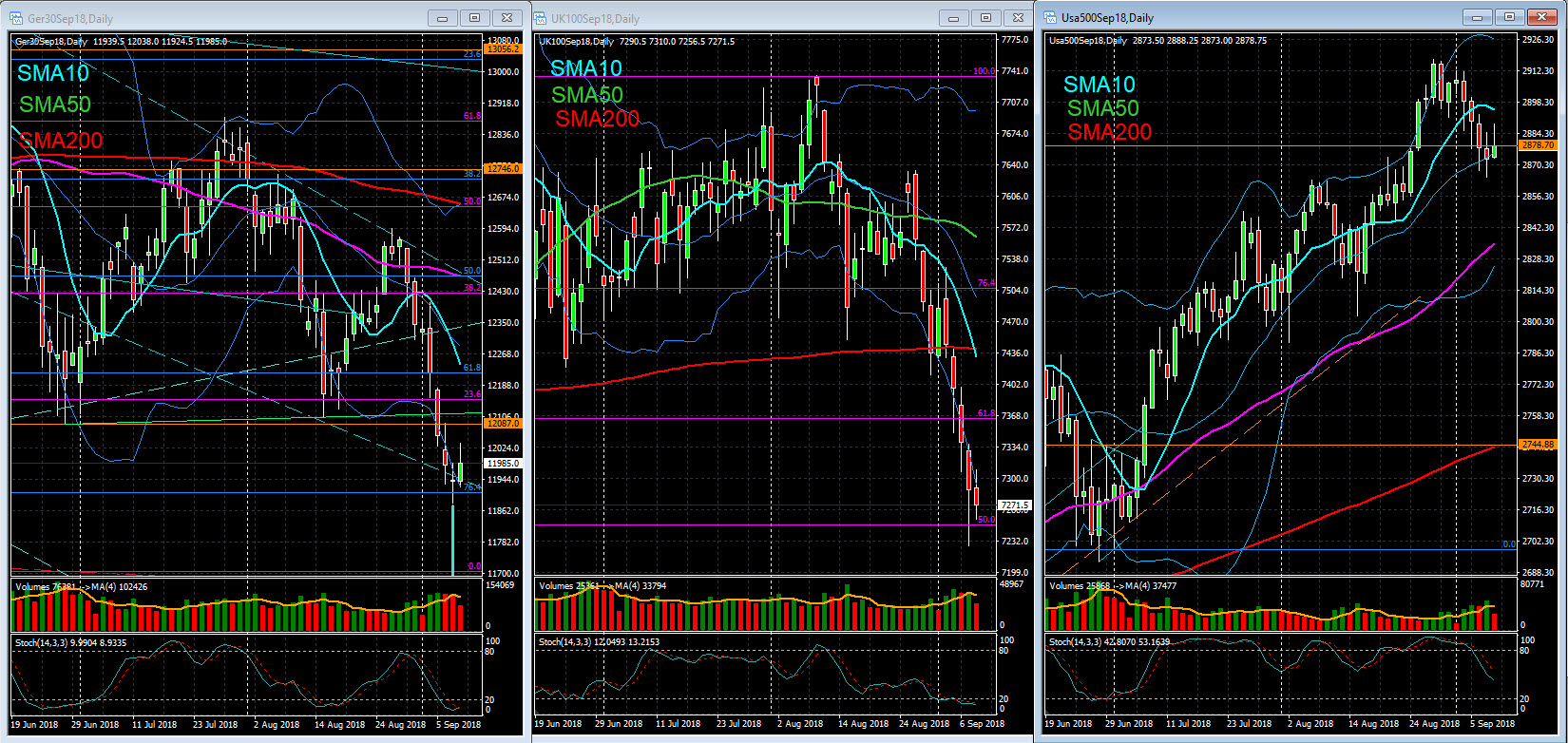

Sep 05, 2018 at 21:09

The behavior of European stock exchanges continues to reflect investors' risk aversion. The day was marked by the start of talks between the US and Canada on a possible revision of the NAFTA agreement. In addition, some of the attention remains diverted to the news about customs tariffs on trade between the US and China. The banking sector was the only one to end up, as opposed to the technology that led the losses in sectoral terms, due to a series of reductions of recommendation. On the other hand, the German pharmaceutical Bayer depreciated, despite having reported a 3.90% increase in the results of the second quarter. In terms of economic indicators, in the Euro Zone, the PMI economic activity index stood at 54.50 in August, slightly above the expected 54.40. The same indicator, but for the services sector, stood at 54.40, as economists estimated. In Germany, the PMI for the services sector reached 55.0, compared to the expected 55.20.

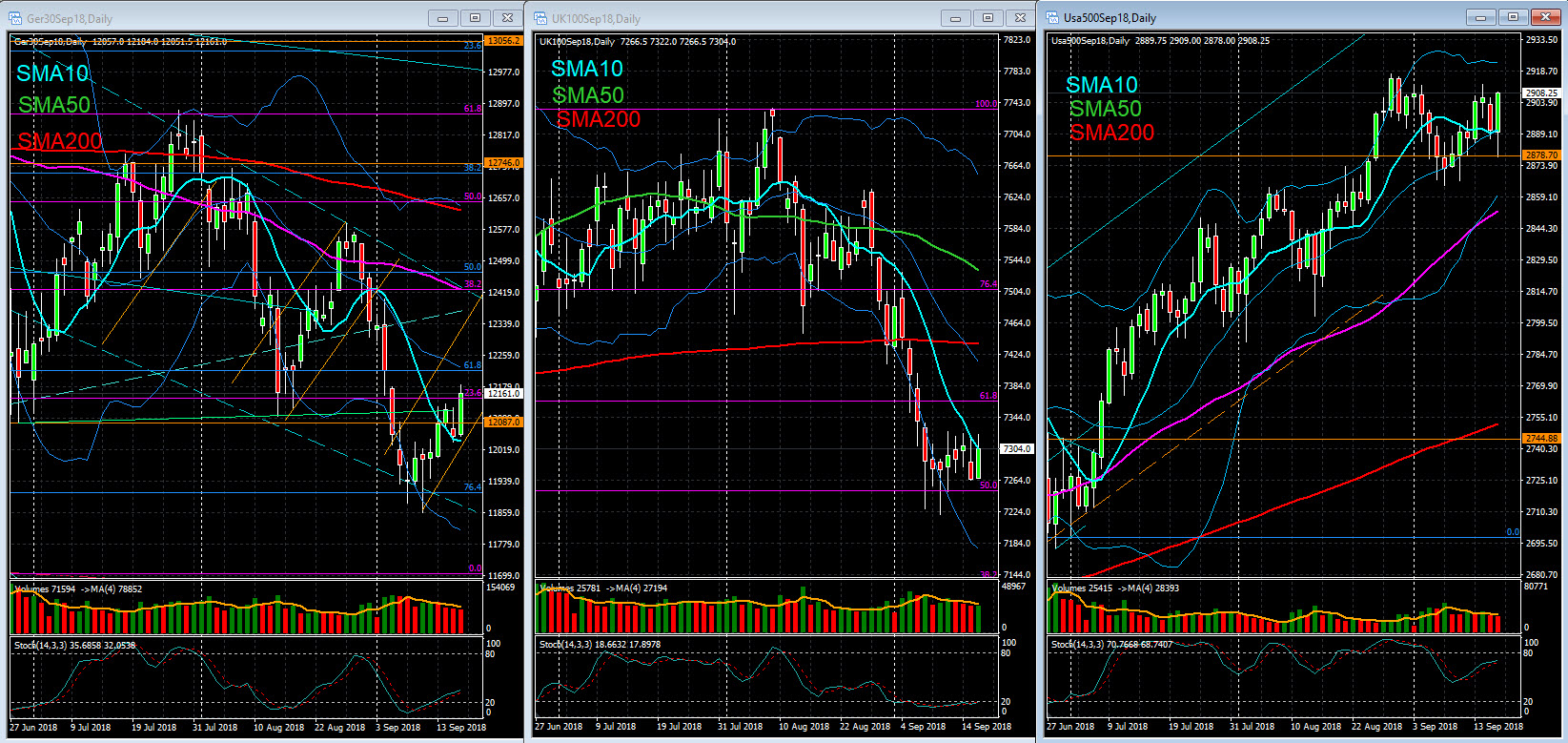

Sep 06, 2018 at 16:25

Stock Markets – Closing Note – 6 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

The trend of European markets in today's session was negative. Pressure from emerging markets as well as fears about US-China customs tariffs remain the main reasons for investors' increased risk aversion. Leading the losses were the technology sector, reflecting the behavior of US counterparts, and producers of raw materials. Above all, at this moment investors are questioning the future of emerging markets, including Argentina. Yesterday, members of the Government said they were confident about the new agreement with the IMF. However, issues related to Brexit remain as background. The German Government has stated that it is prepared for any scenario, including that of a "no-deal". The London Stock Exchange ended today with a loss of 0.91%.

The US market was trading lower, with tech companies' performance negatively impacting the Nasdaq. Highlighting the losses of Amazon and Apple, as well as chip makers, such as Micron Technology. In terms of economic indicators, the ADP employment report showed that 163 000 jobs were created during August, an increase below the expected 200 000. Still on the labor market, the number of weekly applications for unemployment benefits reached 203 000, lower than the estimated 213 000. On the other hand, factory orders decreased 0.80% in July, after two months of increases and against an expected fall of 0.60%. On the other hand, orders for durable goods decreased 1.70% in July, in line with expectations. The ISM index for the services sector stood at 58.5 in August, compared to the previous 55.7 and the forecast 56.8.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

The trend of European markets in today's session was negative. Pressure from emerging markets as well as fears about US-China customs tariffs remain the main reasons for investors' increased risk aversion. Leading the losses were the technology sector, reflecting the behavior of US counterparts, and producers of raw materials. Above all, at this moment investors are questioning the future of emerging markets, including Argentina. Yesterday, members of the Government said they were confident about the new agreement with the IMF. However, issues related to Brexit remain as background. The German Government has stated that it is prepared for any scenario, including that of a "no-deal". The London Stock Exchange ended today with a loss of 0.91%.

The US market was trading lower, with tech companies' performance negatively impacting the Nasdaq. Highlighting the losses of Amazon and Apple, as well as chip makers, such as Micron Technology. In terms of economic indicators, the ADP employment report showed that 163 000 jobs were created during August, an increase below the expected 200 000. Still on the labor market, the number of weekly applications for unemployment benefits reached 203 000, lower than the estimated 213 000. On the other hand, factory orders decreased 0.80% in July, after two months of increases and against an expected fall of 0.60%. On the other hand, orders for durable goods decreased 1.70% in July, in line with expectations. The ISM index for the services sector stood at 58.5 in August, compared to the previous 55.7 and the forecast 56.8.

ไฟล์แนบ :

Sep 07, 2018 at 23:13

Stock Markets – Closing Note – 7 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Most European stock markets closed lower. Investor sentiment has remained conditioned by threats to trade relations between the US and its main partners (European Union, Canada and China). The banking sector remained under pressure. Deutsche Bank shares fell 1.48%, after news that the Chinese group HNA intends to sell its 7.60% stake. On the other hand, IAG's stocks have come down, in reaction to the British Airways statement that a computer-based attack, lasting several days, will have affected 380,000 cards. On the macroeconomic front, Eurostat reported today that the economies of the Eurozone and the European Union grew 2.10% in the second quarter, after 2.10% in the first three months of the year. Compared to the previous quarter, GDP in the Euro Zone and in the EU rose 0.40%.

Wall Street traded slightly without a definite trend, in a session marked by investor reaction to economic data at a time of uncertainty hanging over the US trade negotiations. In terms of economic indicators, the most awaited indicator of the day and week was the employment report, known today before the opening of the session. This publication has raised renewed fears about the conduct of monetary policy by the FED. During August, the US economy created 201,000 jobs, up from 190,000 expected and 157,000 in July, reflecting a growing economy that showed no signs of slowing down during the summer season. The annualized unemployment rate (currently at the lowest of the last 18 years) was 3.90%, down from 3.80% in July, but in line with expectations. But the biggest surprise came from wages, since it was observed in August a monthly increase of 0.40%, higher than the 0.20% forecast and the previous 0.30%. Year-on-year, the increase was 2.90% for the highest since June 2009.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Most European stock markets closed lower. Investor sentiment has remained conditioned by threats to trade relations between the US and its main partners (European Union, Canada and China). The banking sector remained under pressure. Deutsche Bank shares fell 1.48%, after news that the Chinese group HNA intends to sell its 7.60% stake. On the other hand, IAG's stocks have come down, in reaction to the British Airways statement that a computer-based attack, lasting several days, will have affected 380,000 cards. On the macroeconomic front, Eurostat reported today that the economies of the Eurozone and the European Union grew 2.10% in the second quarter, after 2.10% in the first three months of the year. Compared to the previous quarter, GDP in the Euro Zone and in the EU rose 0.40%.

Wall Street traded slightly without a definite trend, in a session marked by investor reaction to economic data at a time of uncertainty hanging over the US trade negotiations. In terms of economic indicators, the most awaited indicator of the day and week was the employment report, known today before the opening of the session. This publication has raised renewed fears about the conduct of monetary policy by the FED. During August, the US economy created 201,000 jobs, up from 190,000 expected and 157,000 in July, reflecting a growing economy that showed no signs of slowing down during the summer season. The annualized unemployment rate (currently at the lowest of the last 18 years) was 3.90%, down from 3.80% in July, but in line with expectations. But the biggest surprise came from wages, since it was observed in August a monthly increase of 0.40%, higher than the 0.20% forecast and the previous 0.30%. Year-on-year, the increase was 2.90% for the highest since June 2009.

ไฟล์แนบ :

Sep 10, 2018 at 18:31

Stock Markets – Closing Note – 10 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Today European stock markets ended positive. The banking sector led the gains, and such performance stood out in the Italian market. Intesa, Unicredit and Banco BPM rose more than 5%. In fact, as a reflection of recent days, several members of the Government of Rome expressed their intention to comply with the Community budgetary rules, the Italian stock market showed a relative overperformance, having registered a valuation of more than 2% and the yields of OT to keep up to a minimum of one month. In the political arena, investors also reacted today to the election results in Sweden and developments related to Brexit.

The US stock exchange started the week on a positive note, with shares of tech companies recovering from losses last week. Even so, attention remains focused on US-China trade relations, after Friday, Donald Trump raised the possibility of applying additional tariffs on Chinese products worth 267 M.USD. However, the US president said that Apple should change its production to the US to avoid being hit by customs tariffs imposed on Chinese imports.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Today European stock markets ended positive. The banking sector led the gains, and such performance stood out in the Italian market. Intesa, Unicredit and Banco BPM rose more than 5%. In fact, as a reflection of recent days, several members of the Government of Rome expressed their intention to comply with the Community budgetary rules, the Italian stock market showed a relative overperformance, having registered a valuation of more than 2% and the yields of OT to keep up to a minimum of one month. In the political arena, investors also reacted today to the election results in Sweden and developments related to Brexit.

The US stock exchange started the week on a positive note, with shares of tech companies recovering from losses last week. Even so, attention remains focused on US-China trade relations, after Friday, Donald Trump raised the possibility of applying additional tariffs on Chinese products worth 267 M.USD. However, the US president said that Apple should change its production to the US to avoid being hit by customs tariffs imposed on Chinese imports.

ไฟล์แนบ :

Sep 11, 2018 at 18:37

Stock Markets – Closing Note – 11 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets have traded slightly today, with most sectors down. The sentiment was conditioned by confirmation by the World Trade Organization that it will respond to China's request for the country to obtain permission to impose sanctions against the US for failing to comply with anti-dumping measures of the international entity. Thus, in face of investors' concerns about the relations between these two countries, commodity producers ended up leading losses in sectoral terms, with a depreciation of around 1%. ArcelorMittal fell 1.98% after news of rising its bid to buy Essar Steel. On the other hand, Apple's suppliers (such as STMicroelectronics) were penalized by the statements of the American President. Donald Trump said that the technology company is being hampered by the tariffs imposed on Chinese imports. Meanwhile, oil prices in the United States rose to levels close to $ 68 a barrel in face of mounting fears about the hurricane approaching the US East Coast that could condition production of this raw material. In terms of economic indicators, in Germany, the ZEW sentiment index of financial agents was better than expected, as it stood at -10.6 in September, compared to the -13.0 expected.

The US market reversed to positive ground after starting lower in today's session. At stake was the performance of the technology sector.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets have traded slightly today, with most sectors down. The sentiment was conditioned by confirmation by the World Trade Organization that it will respond to China's request for the country to obtain permission to impose sanctions against the US for failing to comply with anti-dumping measures of the international entity. Thus, in face of investors' concerns about the relations between these two countries, commodity producers ended up leading losses in sectoral terms, with a depreciation of around 1%. ArcelorMittal fell 1.98% after news of rising its bid to buy Essar Steel. On the other hand, Apple's suppliers (such as STMicroelectronics) were penalized by the statements of the American President. Donald Trump said that the technology company is being hampered by the tariffs imposed on Chinese imports. Meanwhile, oil prices in the United States rose to levels close to $ 68 a barrel in face of mounting fears about the hurricane approaching the US East Coast that could condition production of this raw material. In terms of economic indicators, in Germany, the ZEW sentiment index of financial agents was better than expected, as it stood at -10.6 in September, compared to the -13.0 expected.

The US market reversed to positive ground after starting lower in today's session. At stake was the performance of the technology sector.

ไฟล์แนบ :

Sep 13, 2018 at 01:06

Stock Markets – Closing Note – 12 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock markets closed higher, with most sectors of activity on positive ground. The oil companies were among the best performers, due to the rise in the price of crude oil. On the other hand, in the retail sector, the Spanish Inditex increased 4.11%. After having presented the lowest revenue growth in the last 4 years for the first half of the year, the retailer expects that sales growth will accelerate and that there will be an improvement in profit in the second quarter. In the first six months of the year, the company recorded sales of € 12030 M., compared to estimates of 12060 M.€ and a net profit of 1410 M.€, in line with forecasts. Contrary to the general trend of the markets were the companies of the technological sector and the utilities. In Frankfurt, Deutsche Bank and Commerzbank devalued, after the German magazine Der Spiegel has advanced that the two institutions are increasingly available for a merger. However, Commerzbank CEO Martin Zielke prefers to do the operation "today than tomorrow", while the head of Deutsche Bank has reported internally that this transaction is not on the agenda for the next 18 months.

The US market traded lower, pressured by falling stocks of chip makers. In fact, the technology sector, and more precisely the titles of the semiconductor companies lost ground, the day that Apple will present a new series of products. Despite the secrecy that usually surrounds this presentation, some rumors are already circulating in computer environments. The company is due to introduce a new range of iPhones inspired by the iPhone X. The new iPhones are supposed to be bigger and the screen should cover one of the faces of the new device. One of the biggest unknowns of these new products will be its price. In the last quarter, iPhones revenue growth was almost exclusively due to price increases, as sales only increased by 1%. Now analysts and investors are wondering if the new models will cost more than $ 1,000, the price of iPhone X. In addition, Apple will unveil new versions of MacBook Air, Mac Mini, iPad and Apple Watch.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock markets closed higher, with most sectors of activity on positive ground. The oil companies were among the best performers, due to the rise in the price of crude oil. On the other hand, in the retail sector, the Spanish Inditex increased 4.11%. After having presented the lowest revenue growth in the last 4 years for the first half of the year, the retailer expects that sales growth will accelerate and that there will be an improvement in profit in the second quarter. In the first six months of the year, the company recorded sales of € 12030 M., compared to estimates of 12060 M.€ and a net profit of 1410 M.€, in line with forecasts. Contrary to the general trend of the markets were the companies of the technological sector and the utilities. In Frankfurt, Deutsche Bank and Commerzbank devalued, after the German magazine Der Spiegel has advanced that the two institutions are increasingly available for a merger. However, Commerzbank CEO Martin Zielke prefers to do the operation "today than tomorrow", while the head of Deutsche Bank has reported internally that this transaction is not on the agenda for the next 18 months.

The US market traded lower, pressured by falling stocks of chip makers. In fact, the technology sector, and more precisely the titles of the semiconductor companies lost ground, the day that Apple will present a new series of products. Despite the secrecy that usually surrounds this presentation, some rumors are already circulating in computer environments. The company is due to introduce a new range of iPhones inspired by the iPhone X. The new iPhones are supposed to be bigger and the screen should cover one of the faces of the new device. One of the biggest unknowns of these new products will be its price. In the last quarter, iPhones revenue growth was almost exclusively due to price increases, as sales only increased by 1%. Now analysts and investors are wondering if the new models will cost more than $ 1,000, the price of iPhone X. In addition, Apple will unveil new versions of MacBook Air, Mac Mini, iPad and Apple Watch.

ไฟล์แนบ :

Sep 14, 2018 at 02:28

Stock Markets – Closing Note – 13 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets finished higher on a day marked by the meetings of the Central Banks of Turkey, ECB and England. Producers of raw materials and car manufacturers have benefited from the prospect of renewed talks between the US and China. On the other hand, the technology sector reacted positively to the presentation of new products by Apple. Meanwhile, the price of oil corrected today from the highs of May, after surpassing the 80 USD, due to the possible impact of Hurricane Florence on the North American production. The storm has slowed down and is now in Category 2, thus lowering the impact on barrel production. As expected, the ECB decided to keep the key interest rates unchanged and reiterated its intention to end the asset purchase program later this year. The statement said that the ECB "expects the ECB's key interest rates to remain at current levels, at least until the summer of 2019." At the press conference after the board meeting, Mario Draghi said he has decided to revise his projections for Eurozone growth downward, pointing to increased protectionism and financial market volatility as factors that may weigh on the performance of economy of the region. Mario Draghi kept inflation forecasts at 1.70% between this year and 2020, but cut the growth projections for this year from 2.10% to 2.00%. For 2019, it lowered the forecast of 1.90%, to 1.80%, maintaining only the growth projection for 2020 at 1.70%. Another meeting that caught the attention of investors was that of the Central Bank of Turkey which raised interest rates from 17.75% to 24%. Consequently, the Turkish Lira appreciated significantly against the Dollar. This was a decision that exceeded market forecasts. On the other hand, the Bank of England also decided to keep the principal interest rates at 0.75%.

The US market traded higher, although President Trump said in a tweet that there is no rush to reach an agreement with China. In the business field, Apple was gaining ground, after yesterday the reaction to the presentation of the new products have not been positive. In macroeconomic terms, during August, inflation in annual terms increased 2.70% compared to 2.80% and 2.90% in the previous month. If we exclude the most volatile goods, the consumer price index rose by 2.20% compared to the expected 2.40%.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets finished higher on a day marked by the meetings of the Central Banks of Turkey, ECB and England. Producers of raw materials and car manufacturers have benefited from the prospect of renewed talks between the US and China. On the other hand, the technology sector reacted positively to the presentation of new products by Apple. Meanwhile, the price of oil corrected today from the highs of May, after surpassing the 80 USD, due to the possible impact of Hurricane Florence on the North American production. The storm has slowed down and is now in Category 2, thus lowering the impact on barrel production. As expected, the ECB decided to keep the key interest rates unchanged and reiterated its intention to end the asset purchase program later this year. The statement said that the ECB "expects the ECB's key interest rates to remain at current levels, at least until the summer of 2019." At the press conference after the board meeting, Mario Draghi said he has decided to revise his projections for Eurozone growth downward, pointing to increased protectionism and financial market volatility as factors that may weigh on the performance of economy of the region. Mario Draghi kept inflation forecasts at 1.70% between this year and 2020, but cut the growth projections for this year from 2.10% to 2.00%. For 2019, it lowered the forecast of 1.90%, to 1.80%, maintaining only the growth projection for 2020 at 1.70%. Another meeting that caught the attention of investors was that of the Central Bank of Turkey which raised interest rates from 17.75% to 24%. Consequently, the Turkish Lira appreciated significantly against the Dollar. This was a decision that exceeded market forecasts. On the other hand, the Bank of England also decided to keep the principal interest rates at 0.75%.

The US market traded higher, although President Trump said in a tweet that there is no rush to reach an agreement with China. In the business field, Apple was gaining ground, after yesterday the reaction to the presentation of the new products have not been positive. In macroeconomic terms, during August, inflation in annual terms increased 2.70% compared to 2.80% and 2.90% in the previous month. If we exclude the most volatile goods, the consumer price index rose by 2.20% compared to the expected 2.40%.

ไฟล์แนบ :

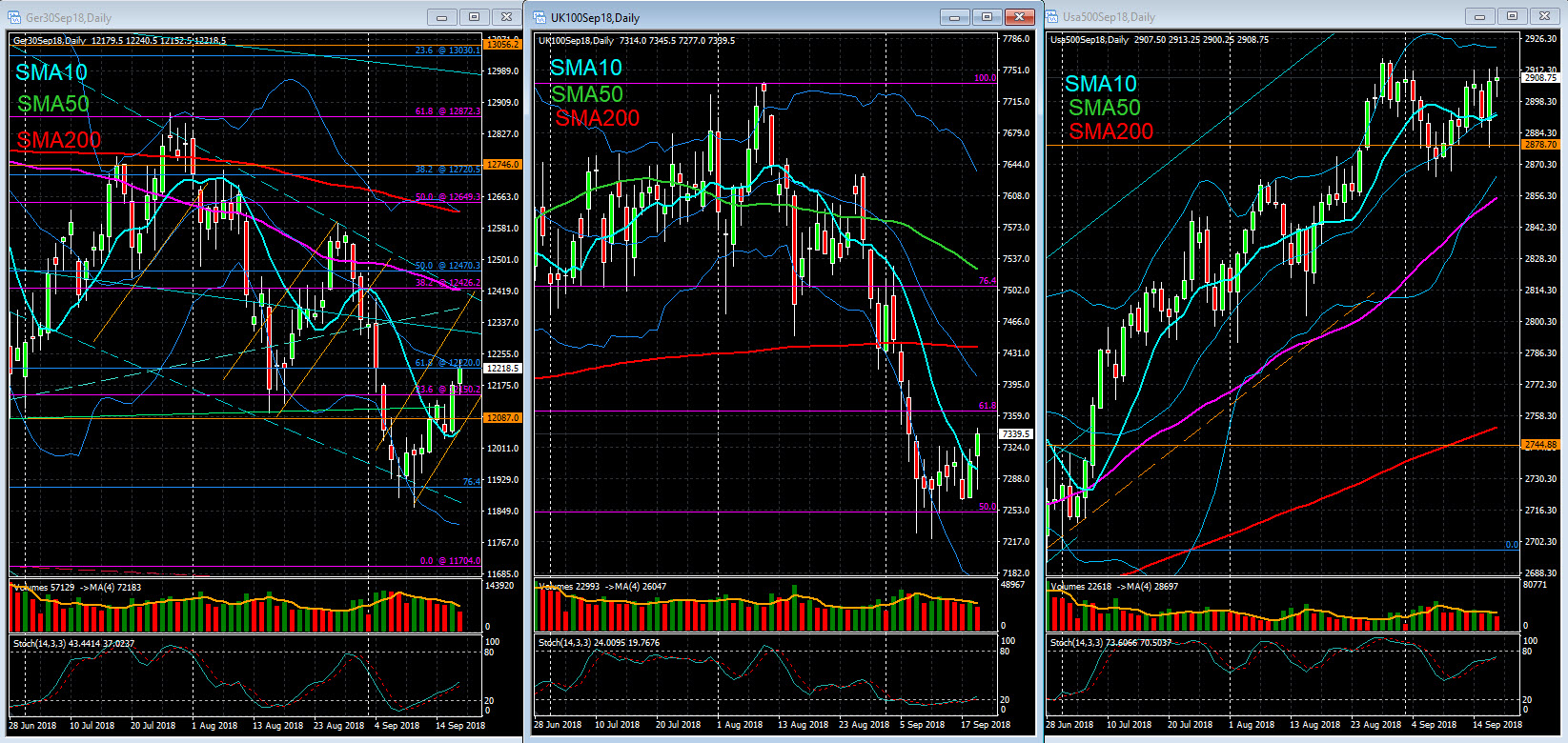

Sep 17, 2018 at 19:17

Stock Markets – Closing Note – 17 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock exchanges traded on a rising trend, despite mounting fears about tensions between the US and China. Producers of raw materials, a sector more sensitive to these issues, ended up slightly after the most recent developments in this area. The retail sector was highlighted, due to the strong valuation carried out by the Swedish H & M. The company advanced more than 16 percent after delivering better-than-expected results: sales reached 55820 M.SEK in the third quarter, against a forecast range of 53220 M.SEK and 55490 M.SEK. The technological sector was among the worst performers, in line with the behavior of the American counterparts. In terms of economic indicators, inflation in the Eurozone in August slowed slightly to 2%, thus confirming the first reading.

The US market began the week low, with sentiment being influenced by the uncertainty associated with growing tensions between the US and China. In addition, at the end of Friday, Bloomberg reported that the Trump Administration would be willing to implement new tariffs on 200,000 M.USD of Chinese products and simultaneously launch a new round of negotiations with Beijing. On Sunday, news in this regard was also given by CNBC. On Saturday, the Wall Street Journal mentioned the additional tariffs on Chinese imports would be 10% rather than 25% as initially thought. The same source referred that Chinese officials would not participate in the talks promoted by Washington if new tariffs on Chinese exports were implemented. At the same time, the technology sector was underperforming as Amazon, Apple and Micron shares lost ground. Amazon was down 1.94%, after one Citibank analyst suggested a two-way split in face of competition issues under Trump's new policies.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock exchanges traded on a rising trend, despite mounting fears about tensions between the US and China. Producers of raw materials, a sector more sensitive to these issues, ended up slightly after the most recent developments in this area. The retail sector was highlighted, due to the strong valuation carried out by the Swedish H & M. The company advanced more than 16 percent after delivering better-than-expected results: sales reached 55820 M.SEK in the third quarter, against a forecast range of 53220 M.SEK and 55490 M.SEK. The technological sector was among the worst performers, in line with the behavior of the American counterparts. In terms of economic indicators, inflation in the Eurozone in August slowed slightly to 2%, thus confirming the first reading.

The US market began the week low, with sentiment being influenced by the uncertainty associated with growing tensions between the US and China. In addition, at the end of Friday, Bloomberg reported that the Trump Administration would be willing to implement new tariffs on 200,000 M.USD of Chinese products and simultaneously launch a new round of negotiations with Beijing. On Sunday, news in this regard was also given by CNBC. On Saturday, the Wall Street Journal mentioned the additional tariffs on Chinese imports would be 10% rather than 25% as initially thought. The same source referred that Chinese officials would not participate in the talks promoted by Washington if new tariffs on Chinese exports were implemented. At the same time, the technology sector was underperforming as Amazon, Apple and Micron shares lost ground. Amazon was down 1.94%, after one Citibank analyst suggested a two-way split in face of competition issues under Trump's new policies.

ไฟล์แนบ :

Sep 18, 2018 at 20:20

Stock Markets – Closing Note – 18 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock markets ended slightly higher at a session where the focus was mostly on recent news reports on US-China trade relations. And it was in this sense that producers of raw materials ended up high. In turn, technology companies benefited from the gains of their US counterparts. In terms of business, Sweden's H&M fell more than 1%, after the strong recovery achieved yesterday after the presentation of results higher than expected. On the macroeconomic front, and as expected, the Hungarian Central Bank kept the key interest rates unchanged at 0.90%.

Wall Street traded bullish, with investors keen on the latest developments regarding trade tensions between the US and China. In addition, the technology sector showed an upward trend, with Apple standing out. Yesterday at the end of the day it was reported that the Trump Administration will apply, from next week, a rate increased by 10% over 200 000 M.USD of Chinese products, which could be increased up to 25% by the end of the year. In addition, a study on the taxation of 250 000 M.USD of other imports from China would be in preparation. However, China has already announced that it will have no choice but to retaliate. On the other hand, investors were also reacting to the figures released by Oracle and FedEx. Oracle reported its quarterly accounts, adjusted adjusted EPS reached 0.71 USD and revenues 9190 M.USD. Analysts had forecast a EPS of 0.69 USD and revenue of 9280 M.USD. The stock lost about 1%. In turn, Global carrier reported a adjusted EPS of 3.46 USD, which fell short of 3.80 USD estimated. The company improved its projections for 2019. The shares fell 4.33%. In terms of indicators, NAHB Housing Market Index, the sentiment index for builders stood at 67 in September, slightly above the expected 66.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European stock markets ended slightly higher at a session where the focus was mostly on recent news reports on US-China trade relations. And it was in this sense that producers of raw materials ended up high. In turn, technology companies benefited from the gains of their US counterparts. In terms of business, Sweden's H&M fell more than 1%, after the strong recovery achieved yesterday after the presentation of results higher than expected. On the macroeconomic front, and as expected, the Hungarian Central Bank kept the key interest rates unchanged at 0.90%.

Wall Street traded bullish, with investors keen on the latest developments regarding trade tensions between the US and China. In addition, the technology sector showed an upward trend, with Apple standing out. Yesterday at the end of the day it was reported that the Trump Administration will apply, from next week, a rate increased by 10% over 200 000 M.USD of Chinese products, which could be increased up to 25% by the end of the year. In addition, a study on the taxation of 250 000 M.USD of other imports from China would be in preparation. However, China has already announced that it will have no choice but to retaliate. On the other hand, investors were also reacting to the figures released by Oracle and FedEx. Oracle reported its quarterly accounts, adjusted adjusted EPS reached 0.71 USD and revenues 9190 M.USD. Analysts had forecast a EPS of 0.69 USD and revenue of 9280 M.USD. The stock lost about 1%. In turn, Global carrier reported a adjusted EPS of 3.46 USD, which fell short of 3.80 USD estimated. The company improved its projections for 2019. The shares fell 4.33%. In terms of indicators, NAHB Housing Market Index, the sentiment index for builders stood at 67 in September, slightly above the expected 66.

ไฟล์แนบ :

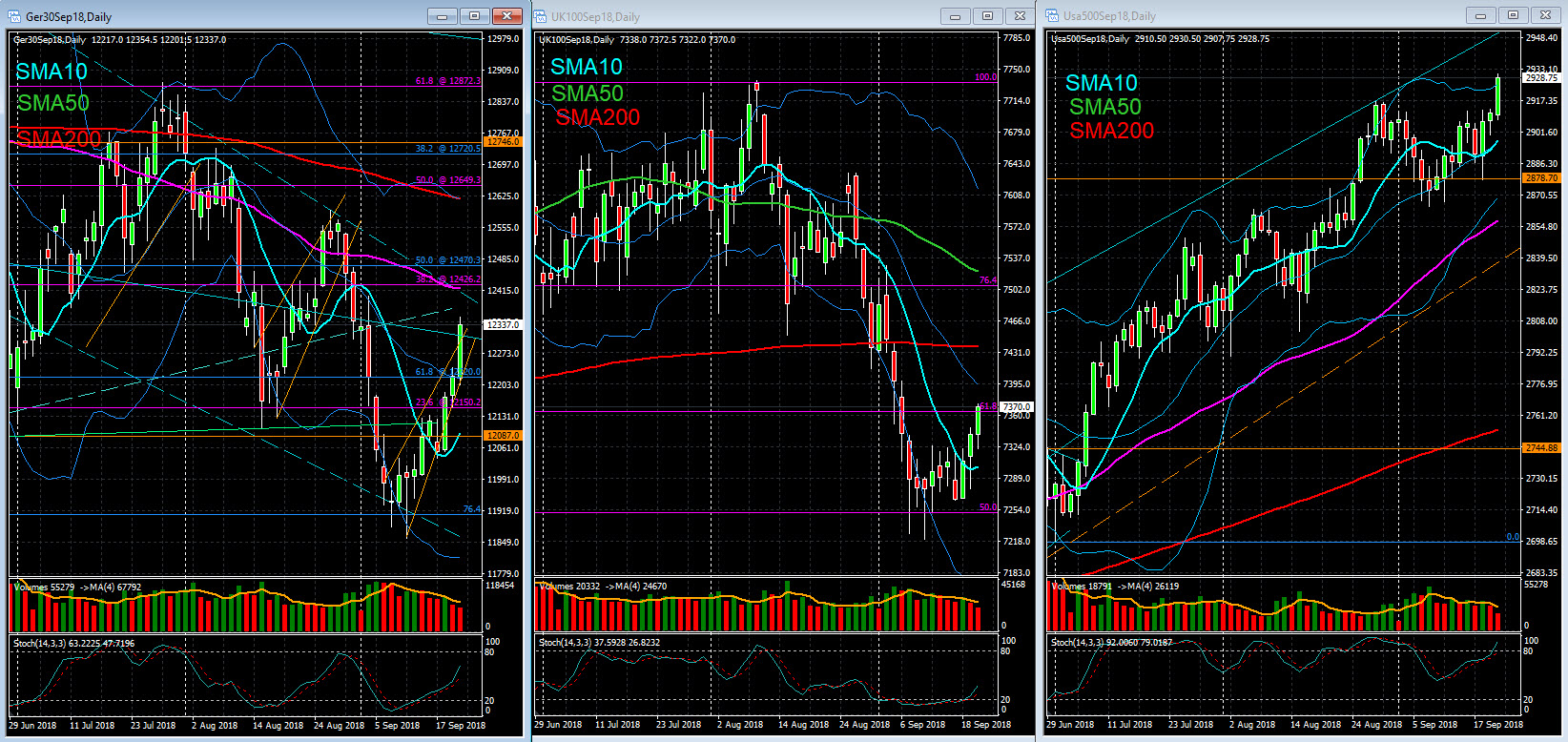

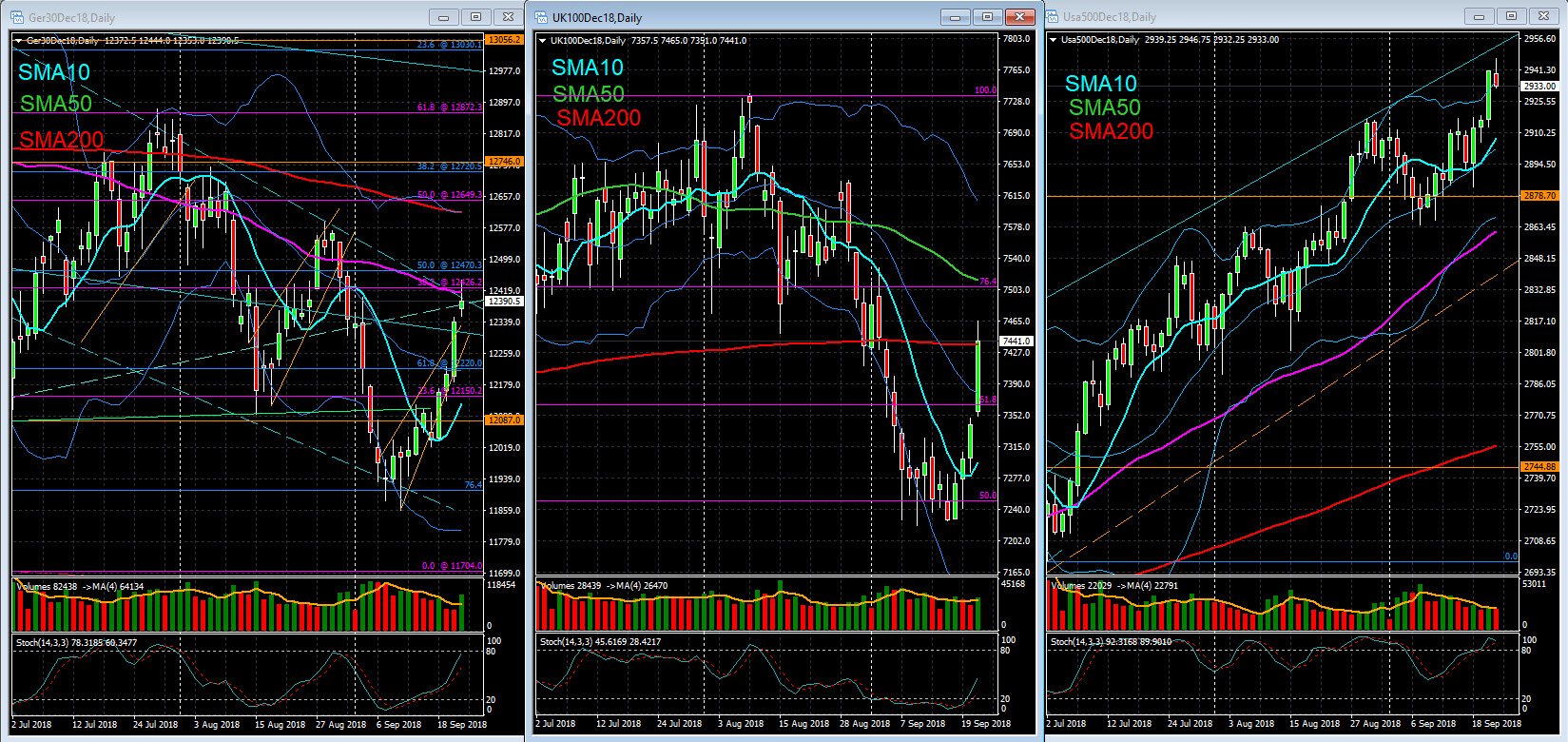

Sep 19, 2018 at 18:08

Stock Markets – Closing Note – 19 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

In today's session, European markets have ended up in face of an illusion of calm regarding the trade tensions between the US and China. The producers of raw materials have already reflected this greater optimism, gaining more than 3%. The day was also marked by rising zinc and nickel prices. Of note are the valuations of the mining companies, such as Glencore, Antofagasta, Anglo American and Billiton. At the same time, car manufacturers and banks also posted gains of more than 1%. Automobile sales grew by almost 30% in Europe during the month of August compared to the same period in 2017. This strong increase is partly explained by the fact that the new European rules concerning gas emissions for car manufacturers came into force in September.

The US market traded in different directions, with the technology sector reporting slight losses, but the Dow Jones and S & P500 had earnings. China's retaliation for the US announcement lessened the fears of investors whose uncertainty has influenced investors' decisions. It should be recalled that following the Trump Administration's announcement that it would implement a rate of 10% over 200,000 M.USD (which could reach 25% by the end of the year), China retaliated by imposing on exports (60,000 M.USD ) a 10% rate. The Chinese retaliation appears to be less than the amount of Chinese products that will be subject to American tariffs. In terms of economic indicators, the current account deficit decreased by 17% in the second quarter from 121700 M.USD to 101500 M.USD, the lowest of the last 3 years. Estimates pointed to a higher deficit (103400 M.USD). On the other hand, the houses under construction increased by 9.20% in August to a total of 1.28 million, up from 1.23 million homes planned. Allocation of building permits during the same month disappointed the market, as the number of licenses decreased 5.70% compared to July and to forecasts of a rise of 0.50%. With respect to the debt market, 10-year TO yields have exceeded 3% for peaks of the last 4 months.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

In today's session, European markets have ended up in face of an illusion of calm regarding the trade tensions between the US and China. The producers of raw materials have already reflected this greater optimism, gaining more than 3%. The day was also marked by rising zinc and nickel prices. Of note are the valuations of the mining companies, such as Glencore, Antofagasta, Anglo American and Billiton. At the same time, car manufacturers and banks also posted gains of more than 1%. Automobile sales grew by almost 30% in Europe during the month of August compared to the same period in 2017. This strong increase is partly explained by the fact that the new European rules concerning gas emissions for car manufacturers came into force in September.

The US market traded in different directions, with the technology sector reporting slight losses, but the Dow Jones and S & P500 had earnings. China's retaliation for the US announcement lessened the fears of investors whose uncertainty has influenced investors' decisions. It should be recalled that following the Trump Administration's announcement that it would implement a rate of 10% over 200,000 M.USD (which could reach 25% by the end of the year), China retaliated by imposing on exports (60,000 M.USD ) a 10% rate. The Chinese retaliation appears to be less than the amount of Chinese products that will be subject to American tariffs. In terms of economic indicators, the current account deficit decreased by 17% in the second quarter from 121700 M.USD to 101500 M.USD, the lowest of the last 3 years. Estimates pointed to a higher deficit (103400 M.USD). On the other hand, the houses under construction increased by 9.20% in August to a total of 1.28 million, up from 1.23 million homes planned. Allocation of building permits during the same month disappointed the market, as the number of licenses decreased 5.70% compared to July and to forecasts of a rise of 0.50%. With respect to the debt market, 10-year TO yields have exceeded 3% for peaks of the last 4 months.

ไฟล์แนบ :

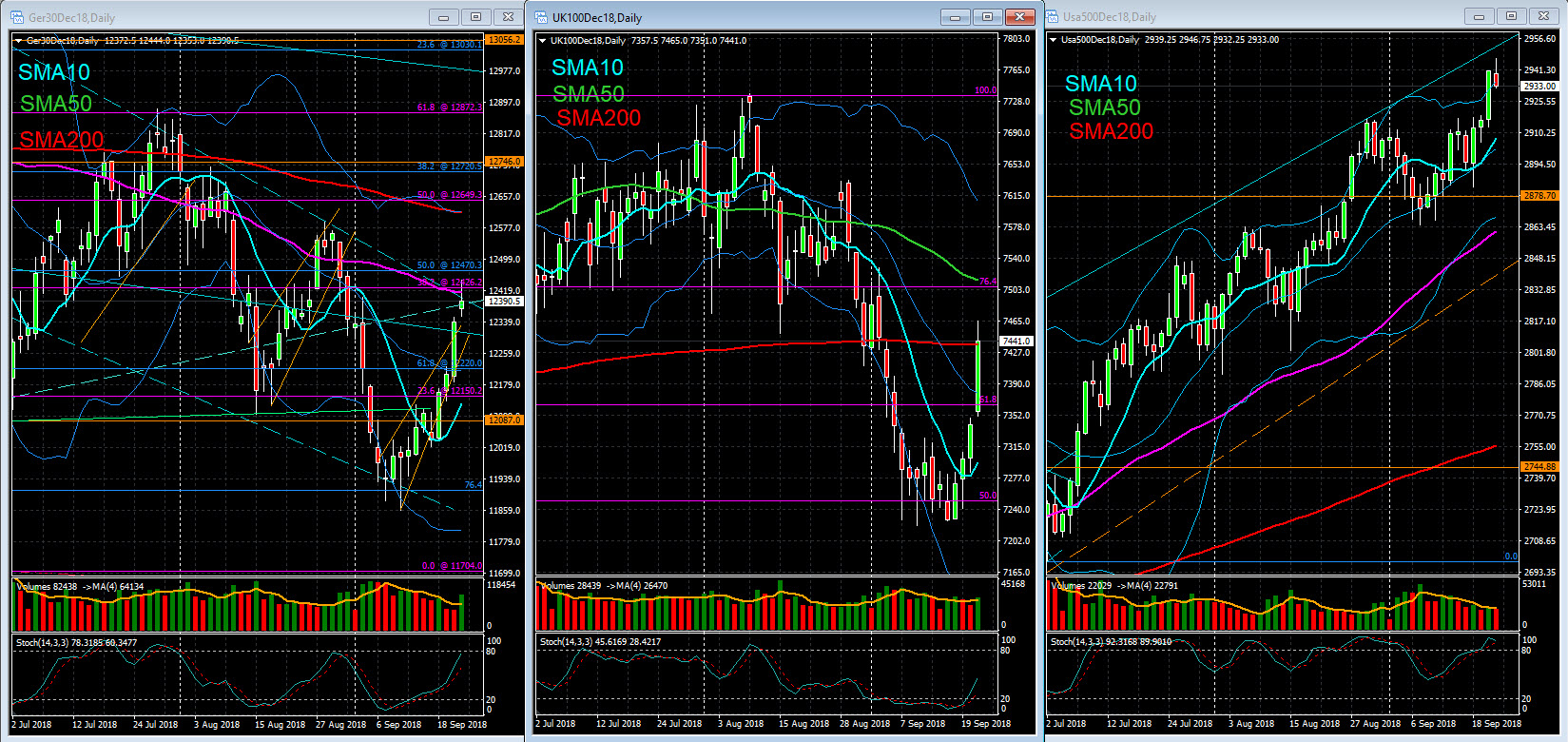

Sep 21, 2018 at 02:20

Stock Markets – Closing Note – 20 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets closed higher, boosted by the behavior of the US market that was influenced by tension decrease regarding the trade war between the US and China. The highlight was for oil, as Donald Trump once again used the social network tweeter to demand the immediate reduction of prices of this raw material. The US President said that the Middle East countries continue to raise oil prices and left a warning about their safety: "We shall remember". This warning of Donald Trump arrives just days before the meeting of the delegates of OPEC, scheduled for this Sunday. Following this meeting, the formal meeting of ministers from the countries of that organization will follow. In international markets, the price of oil fell, with Brent down about 0.90%.

Wall Street traded higher, for the reasons already mentioned and with the banking sector to favor the indices. Banks were favored by the 10-year yield increase of OTs (which exceeded 3.09%). Goldman Sachs, JP Morgan and Bank of America led the gains. On the macroeconomic front, the number of weekly applications for unemployment benefits reached 201,000, compared to 210,000 expected and 204,000 previously. On the other hand, the Philadelphia Fed's activity index stood at 22.9 in September, quite a bit higher than 11.9 in August and 18.0 forecasted by economists. In August, the economy's advanced indicators increased by 0.40%, higher than the estimated 0.50%. On the real estate market, sales of used homes last month remained unchanged relative to July, reaching 5.34 million homes. Economists pointed to an increase of 0.50% for the 5.37 million houses.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets closed higher, boosted by the behavior of the US market that was influenced by tension decrease regarding the trade war between the US and China. The highlight was for oil, as Donald Trump once again used the social network tweeter to demand the immediate reduction of prices of this raw material. The US President said that the Middle East countries continue to raise oil prices and left a warning about their safety: "We shall remember". This warning of Donald Trump arrives just days before the meeting of the delegates of OPEC, scheduled for this Sunday. Following this meeting, the formal meeting of ministers from the countries of that organization will follow. In international markets, the price of oil fell, with Brent down about 0.90%.

Wall Street traded higher, for the reasons already mentioned and with the banking sector to favor the indices. Banks were favored by the 10-year yield increase of OTs (which exceeded 3.09%). Goldman Sachs, JP Morgan and Bank of America led the gains. On the macroeconomic front, the number of weekly applications for unemployment benefits reached 201,000, compared to 210,000 expected and 204,000 previously. On the other hand, the Philadelphia Fed's activity index stood at 22.9 in September, quite a bit higher than 11.9 in August and 18.0 forecasted by economists. In August, the economy's advanced indicators increased by 0.40%, higher than the estimated 0.50%. On the real estate market, sales of used homes last month remained unchanged relative to July, reaching 5.34 million homes. Economists pointed to an increase of 0.50% for the 5.37 million houses.

ไฟล์แนบ :

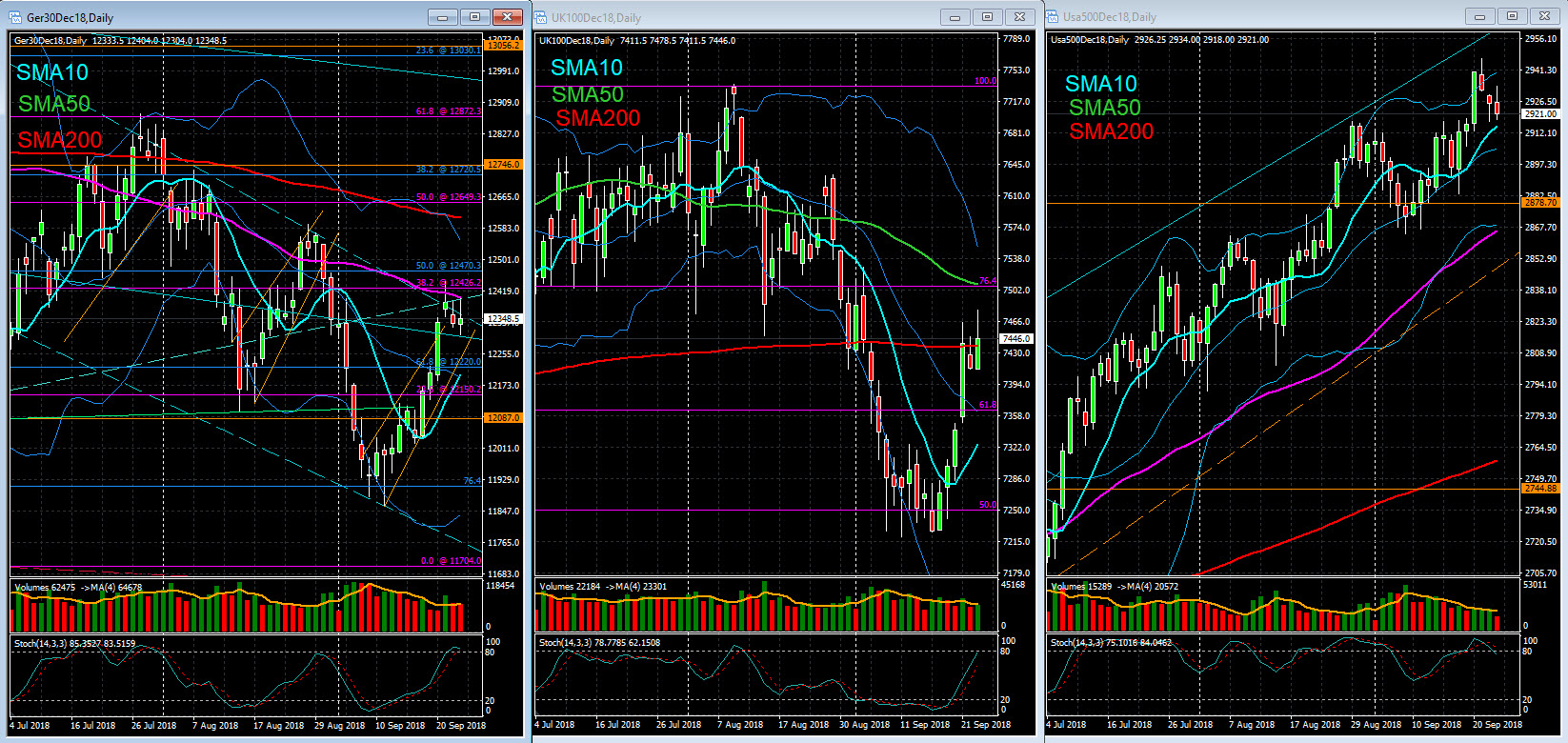

Sep 21, 2018 at 20:44

Stock Markets – Closing Note – 21 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

The last session of the week presented solid gains for the European markets, with the London stock market standing out with an overperformance. The theme of Brexit remains in the sights of investors. Yesterday, at the end of the informal summit hosted by European leaders in Salzburg, no concrete news emerged regarding the negotiation of the EU's relationship with the United Kingdom. With about six months to go before Brexit, which is still undergoing a transitional period until December 2020, European leaders were largely united in the warnings made to the UK. Already today, Theresa May said that discussions on Brexit between the UK and the EU are at an “impasse". The British prime minister added that she will not revoke the outcome of the referendum held in 2016. The British Pound reached the session minimum after this speech. In sectoral terms, and once again, producers of raw materials (including mining companies) made gains on a day marked by rising copper and nickel prices. In terms of economic indicators, the PMI economic activity index for the Euro Zone stood at 54.20 in September, compared to the estimated 54.5. The same indicator, but for the manufacturing sector, it stood at 53.3 (vs. 54.5 forecasted), while for the services sector it reached 54.7 (vs. 54.4 expected).

Wall Street traded higher, with the Dow Jones and S&P500 indexes renewing record highs. McDonald's rose more than 2 percent after the company raised its quarterly dividend by 14.90 percent to 1.16 USD per share. Micron shares fell about 3.50 % after the company cut its revenue estimates, reviving fears about declining demand for chips. Investors were also focused on the operations related to the maturity of futures and options, called the quadruple witching.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

The last session of the week presented solid gains for the European markets, with the London stock market standing out with an overperformance. The theme of Brexit remains in the sights of investors. Yesterday, at the end of the informal summit hosted by European leaders in Salzburg, no concrete news emerged regarding the negotiation of the EU's relationship with the United Kingdom. With about six months to go before Brexit, which is still undergoing a transitional period until December 2020, European leaders were largely united in the warnings made to the UK. Already today, Theresa May said that discussions on Brexit between the UK and the EU are at an “impasse". The British prime minister added that she will not revoke the outcome of the referendum held in 2016. The British Pound reached the session minimum after this speech. In sectoral terms, and once again, producers of raw materials (including mining companies) made gains on a day marked by rising copper and nickel prices. In terms of economic indicators, the PMI economic activity index for the Euro Zone stood at 54.20 in September, compared to the estimated 54.5. The same indicator, but for the manufacturing sector, it stood at 53.3 (vs. 54.5 forecasted), while for the services sector it reached 54.7 (vs. 54.4 expected).

Wall Street traded higher, with the Dow Jones and S&P500 indexes renewing record highs. McDonald's rose more than 2 percent after the company raised its quarterly dividend by 14.90 percent to 1.16 USD per share. Micron shares fell about 3.50 % after the company cut its revenue estimates, reviving fears about declining demand for chips. Investors were also focused on the operations related to the maturity of futures and options, called the quadruple witching.

ไฟล์แนบ :

Sep 24, 2018 at 18:45

Stock Markets – Closing Note – 24 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

On the day the 10% tariff on 200,000 M.USD of Chinese goods entering the United States became a reality, European stock markets ended in negative territory. Most sectors closed lower, with companies in the utilities sector ranking among the worst performers. As in the US, the major European oil companies were favored by rising crude oil prices in international markets. In London, Sky advanced 8.58%. Comcast won the auction for the purchase of Sky, having made a bid higher than the one from Fox at USD 2 per share, that is, 39,000 M.USD. Sky's management has already advised shareholders to accept the selling proposition. In terms of economic indicators, the IFO economic sentiment index reached 103.7 in September, above the forecast 103.2, but slightly lower than the previous 103.80. At a financial event in Brussels, the President of the ECB said that "underlying inflation is expected to grow further over the coming months as a tighter labor market is boosting wage growth." The ECB estimates that the inflation rate in the Euro Zone will remain around 1.70% by 2020. After these statements, the Euro appreciated against the Dollar for highs since mid-June.

The US market was trading lower, pressured by escalating trade tensions between the US and China. Over the weekend, it was reported that the Chinese delegation, which would prepare a new round of negotiations proposed by Washington, canceled its trip. This delegation would precede the main delegation led by Deputy Prime Minister Liu He. Meanwhile, the rhetoric of the Trump Administration has taken on more bellicose tones, such as Secretary of State Mike Pompeo saying that the US is in a "trade war" with China (which lasts for several years) and that his country "will beat it ". In addition, news of the alleged dismissal of US Deputy General Attorney Rod Rosenstein also added to the market's losses. In the business field, the Nasdaq traded lower, pressured by falling shares of Amazon, Facebook, Alphabet and Apple. The oil sector benefited from the oil price hike to highs since 2014 (above $ 80 per barrel), after the meeting held yesterday, cartel members and Russia were satisfied with the balance between supply and demand. demand, not showing any urgency in increasing production.

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

On the day the 10% tariff on 200,000 M.USD of Chinese goods entering the United States became a reality, European stock markets ended in negative territory. Most sectors closed lower, with companies in the utilities sector ranking among the worst performers. As in the US, the major European oil companies were favored by rising crude oil prices in international markets. In London, Sky advanced 8.58%. Comcast won the auction for the purchase of Sky, having made a bid higher than the one from Fox at USD 2 per share, that is, 39,000 M.USD. Sky's management has already advised shareholders to accept the selling proposition. In terms of economic indicators, the IFO economic sentiment index reached 103.7 in September, above the forecast 103.2, but slightly lower than the previous 103.80. At a financial event in Brussels, the President of the ECB said that "underlying inflation is expected to grow further over the coming months as a tighter labor market is boosting wage growth." The ECB estimates that the inflation rate in the Euro Zone will remain around 1.70% by 2020. After these statements, the Euro appreciated against the Dollar for highs since mid-June.

The US market was trading lower, pressured by escalating trade tensions between the US and China. Over the weekend, it was reported that the Chinese delegation, which would prepare a new round of negotiations proposed by Washington, canceled its trip. This delegation would precede the main delegation led by Deputy Prime Minister Liu He. Meanwhile, the rhetoric of the Trump Administration has taken on more bellicose tones, such as Secretary of State Mike Pompeo saying that the US is in a "trade war" with China (which lasts for several years) and that his country "will beat it ". In addition, news of the alleged dismissal of US Deputy General Attorney Rod Rosenstein also added to the market's losses. In the business field, the Nasdaq traded lower, pressured by falling shares of Amazon, Facebook, Alphabet and Apple. The oil sector benefited from the oil price hike to highs since 2014 (above $ 80 per barrel), after the meeting held yesterday, cartel members and Russia were satisfied with the balance between supply and demand. demand, not showing any urgency in increasing production.

ไฟล์แนบ :