Gold and equities retreat from recent peaks

Gold loses altitude

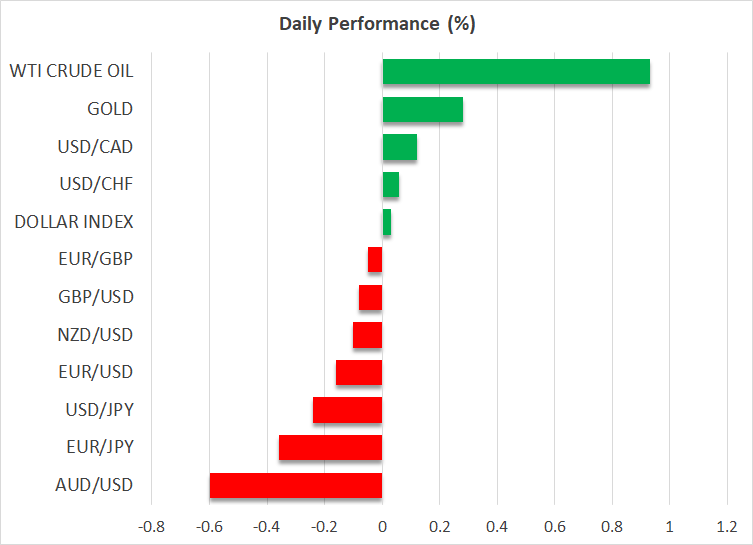

The world’s oldest safe-haven asset started the week in an explosive manner, shooting up to new record highs only to get rejected and close the session sharply lower. The intraday range in gold prices was $115 per ounce yesterday, which amounts to more than 5% of the precious metal’s value.

Behind this reversal lies a tsunami of profit-taking, driven by the recovery in the US dollar and real bond yields, both factors that dampen buying appetite for gold as the metal is priced in dollars and does not pay any interest to hold.

Although the broader trend in gold still appears bullish, the inability to sustain the momentum and the sudden turnaround are sources of concern from a chart perspective, painting a picture of a blow-off top. Hence, further declines cannot be ruled out, in which case the spotlight could shift towards the $2,008 region.

Moving forward, the performance of gold will be decided by a blend of geopolitics, the path of interest rates, direct central bank purchases, and how the economic landscape evolves. In this sense, the coming year could be a fertile period for gold as the global economy loses steam and central banks enter an easing cycle.

The biggest downside risk for gold might be a peace negotiation in Ukraine that exhausts geopolitical demand, although that’s probably a story that requires a change of leadership in the US elections next year.

Dollar recovers some ground

A wave of euro weakness continues to sweep through the FX market, with the single currency suffering at the hands of a softer data pulse and speculation that the European Central Bank will spearhead the global campaign of rate cuts next year. By most counts, the Eurozone is already in a technical recession and with inflation rolling off, there isn’t much standing in the way of ECB rate cuts.

The dollar and the euro are often described as opposite sides of the same coin, so it was natural to see the greenback mount a recovery yesterday as the euro struggled, especially when considering the rebound in US yields. Whether this recovery is sustained will depend on the upcoming US data releases today, which include the JOLTS report and the ISM services survey.

Elsewhere, the Australian dollar got knocked down today after the Reserve Bank toned down its tightening bias, signaling increased uncertainty about whether interest rates will need to be raised any further. On the bright side though, the latest business surveys from China painted a picture of a services sector that is healing, helping to prevent any deeper losses in the China-sensitive Australian dollar.

Stock markets turn down

Shares on Wall Street encountered some rare turbulence this week, with the S&P 500 falling by 0.5% and the tech-heavy Nasdaq losing 1% on Monday. Of course this follows an astonishingly strong performance in November for these indices, driven by hopes for a soft landing, so this retreat is merely a blip on the radar.

In a nutshell, stock markets are currently priced for perfection. Valuations are historically stretched with the S&P 500 trading for 19x forward earnings while profitability assumptions seem overly optimistic with analysts projecting upwards of 11% earnings growth next year, heading into what is likely to be an economic slowdown.

Therefore, the notion of a soft landing is already fully priced into share prices, which leaves scope for disappointment in case reality do esn’t match these rosy expectations, especially when considering that markets tend to underperform in the year leading into a US presidential election.

esn’t match these rosy expectations, especially when considering that markets tend to underperform in the year leading into a US presidential election.

.jpg "Gold and equities retreat from recent peaks")

Currencies Steady Ahead of Fed; UK CPI Holds, Oil Pressured | 17th September 2025

BNB reaching new heights while BTC awaits FOMC

Fed cut expected, market reaction hinges on multiple factors

EBC Markets Briefing | Euro hits 4-year peak despite France downgrade

EUR/USD Hits Four-Year High: All Eyes on the Fed

EUR/USD hits 4-year high amid Fed rate cut expectations

ATFX Market Outlook 17th September 2025