Advertisement

Forex Cyborg

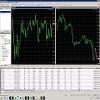

| Zisk : | +190.79% |

| Čerpanie | 19.88% |

| Pipy: | 6076.3 |

| Obchodníci | 2941 |

| Vyhrané: |

|

| Prehrané: |

|

| Typ: | Reálny |

| Páka: | 1:200 |

| Obchodovanie: | Automaticky |

Forex Cyborg Diskusia

Členom od Nov 26, 2016

93 príspevkov

Jan 18, 2018 at 18:03

cool, thanks, so I will increase that ;-)

Členom od Feb 16, 2011

208 príspevkov

Jan 19, 2018 at 08:46

EA trades very bad, uses martingale.

Prílohy:

Členom od Nov 26, 2016

93 príspevkov

Jan 19, 2018 at 10:13

What are you talking about?

I think this post should have gone to FluidTrader.

ForexCyborg doesn't use any martingale.

I think this post should have gone to FluidTrader.

ForexCyborg doesn't use any martingale.

Členom od Jun 30, 2017

25 príspevkov

Jan 21, 2018 at 07:25

Hello Yury48,

You posted a screenshot of FluridTrader and not Forex Cyborg.

Forex Cyborg don't use any kind of grid or martingale strategy.

We high don't recommend to use EAs that use such strategies.

Best regards,

Forex Cyborg Team

You posted a screenshot of FluridTrader and not Forex Cyborg.

Forex Cyborg don't use any kind of grid or martingale strategy.

We high don't recommend to use EAs that use such strategies.

Best regards,

Forex Cyborg Team

Členom od Dec 25, 2016

25 príspevkov

Jan 21, 2018 at 07:25

Which EA is that? FluidTrader? Why do you post it here?

Členom od Feb 16, 2011

208 príspevkov

Jan 21, 2018 at 07:30

Sorry, I really confused the topic.

Členom od Feb 16, 2011

208 príspevkov

Jan 21, 2018 at 07:32

ForexCyborg trades very good.

Členom od Feb 16, 2011

208 príspevkov

Jan 21, 2018 at 08:00

It was a mistake.

Členom od Jul 19, 2017

1 príspevkov

Jan 25, 2018 at 07:12

One of the best commercial EA. I made about 100% profit during 6 month, with acceptable risk and drawdown. So I paid out all my profit and my account is running risk-free now :-) Thanks to ForexCyborg, good job!

Členom od Jun 30, 2017

25 príspevkov

Jan 30, 2018 at 07:12

@sebabahn

Thank you for your very positive feedback!

@all

The first 100% was reached in less than 9 months, even with a 25% DD. I'm quite happy and looking forward for the next 100%

Thank you for your very positive feedback!

@all

The first 100% was reached in less than 9 months, even with a 25% DD. I'm quite happy and looking forward for the next 100%

*Komerčné použitie a spam nebudú tolerované a môžu viesť k zrušeniu účtu.

Tip: Uverejnením adresy URL obrázku /služby YouTube sa automaticky vloží do vášho príspevku!

Tip: Zadajte znak @, aby ste automaticky vyplnili meno používateľa, ktorý sa zúčastňuje tejto diskusie.