Dollar stabilizes amidst mixed risk sentiment

Mideast truce holds, oil struggles

As the shortened one-day NATO summit is underway today, investors are settling into the newly found ceasefire in the Middle East, overlooking violations from either side, as both the Israeli and Iranian administrations claim victory. The truce remains fragile and will most likely be tested over the next days, with the risk of a relapse being quite high.

With equity indices benefiting from the prevailing risk-on sentiment, and the S&P 500 being already 2.5% up this week and within touching distance of the all-time high of 6,147, the oil market is desperately trying to find its footing. The double digit increase since June 13 has swiftly evaporated, with WTI oil now trading at $65, as both consumers and central banks are breathing a sigh of relief ahead of the summer.

Fed, tariffs and budget bill

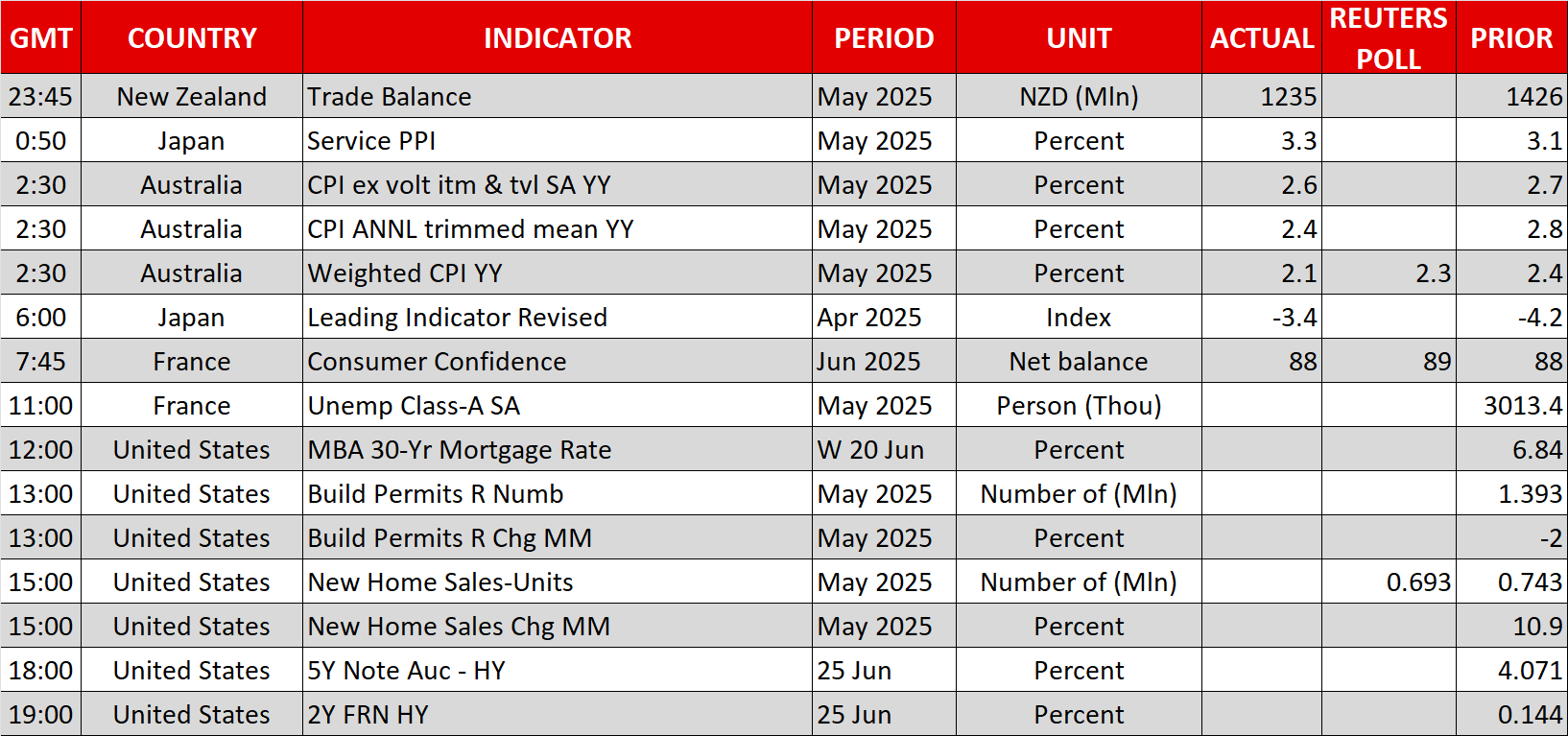

Notably, the safe haven bid that boosted the US dollar for a few sessions has diminished, with the greenback on the back foot again as investors refocus on the non-geopolitical agenda. Euro/dollar is up 0.8% this week, the ailing pound is gaining 1.2% against the dollar, and dollar/yen touched 145. Japan’s stronger services PPI report and the slightly more hawkish mini-minutes from the June BoJ meeting have failed to support the yen.

While Trump appears to control developments on the foreign policy arena, he is unlikely to be content with the considerable lack of progress on key issues such as monetary policy, the budget bill and tariffs.

Fed Chair Powell will deliver his testimony to the Senate Banking Committee today, with the message being identical to Tuesday’s appearance before the House Financial Services committee. A solid US economy is allowing the FOMC to maintain its current monetary stance, while waiting for further information about the budget bill and tariffs.

While Powell kept that door open to rate cuts during 2025 - given that most policy makers are open to such an action - he shut the door to a July rate cut, as put forward by Fed Governors Waller and Bowman in recent days. However, Powell acknowledged that if inflation fails to accelerate aggressively, rate cuts could come sooner. Markets are currently fully pricing in a 25bps rate cut in September and a total of 60bps of easing during 2025.

Asked about the expected timing of the impact of tariffs, Powell responded that a meaningful inflation effect could be seen from June onwards, thus increasing the focus on the next CPI and PCE reports. If this proves to be the case and inflation accelerates over the summer, FOMC members will feel vindicated for having resisted pressure from the US administration to cut rates.

Deadlines loom, newsflow to pick up

With the July 4 deadline set by Republicans fast approaching, the Senate plans a vote of the US budget bill on Friday. At this stage, the outcome is unclear, with a likely failure forcing Senators and the US administration back to the negotiating table. A short delay for further negotiations is possible, potentially even necessary, for an agreement, further denting the current weak attractiveness of the dollar.

Speaking of deadlines, the 90-day pause on reciprocal tariffs will end on July 9, just two weeks away, with sources close to the US administration paving the way for a number of trade deals being announced soon. White House Adviser Hassett concurred by stating that “we will see a sequence of trade deals around the 4th of July. The administration has been focused on getting the One Big Beautiful Bill passed through Congress”.

While US officials continue to negotiate with Japan, South Korea, Vietnam and the EU, investors view another extension as almost certain. However, Trump might first choose to employ this familiar guidebook, threatening the affected countries with triple-digit tariffs, which could potentially unsettle risk markets once again.

.jpg "Dollar stabilizes amidst mixed risk sentiment")

Gold stabilised at $4,000, but the upward trend has already broken down

The dollar risks losing support from tariff revenues

The dollar risks losing support from tariff revenues

ZEC as the omen of a brewing storm in crypto

ZEC as the omen of a brewing storm in crypto

Risk markets struggle on lack of bullish catalysts

Supreme Court's Tariff Battle: A Turning Point or More Uncertainty for Global Trade?