Fed awaited as stocks jump, dollar slips after US CPI

- Dollar pressured from in-line CPI report as stocks extend rally

- But Fed rate cut expectations pared back slightly ahead of new Fed dot plot

- Fed to kickstart central bank bonanza

Markets upbeat after CPI report as all eyes turn to Fed

The Federal Reserve will kick off the barrage of central meetings on Wednesday as policymakers set interest rates for the final time in 2023. The European Central Bank, Bank of England and Swiss National Bank will announce their decisions on Thursday before the Bank of Japan wraps things up next Tuesday.

With inflation seemingly coming under control in all jurisdictions, investors are gearing up for the first explicit signals of a dovish pivot. However, it’s likely that policymakers will only go as far as flagging the end of the tightening cycle, so there is significant room for disappointment, especially if the Fed’s latest dot plot doesn’t pencil in as many rate cuts for 2024 as traders have.

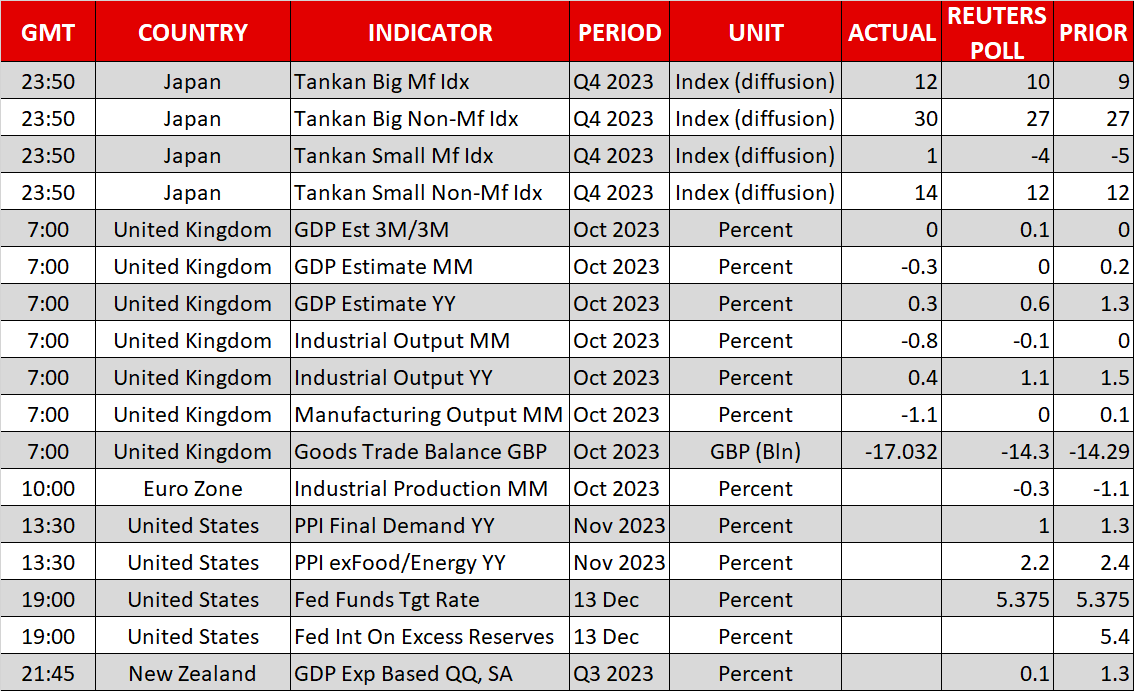

Ahead of the Fed’s decision, due at 19:00 GMT, the November CPI report did little to dampen speculation about aggressive rate cuts on Tuesday. Headline inflation in the US eased slightly to 3.1% y/y but the month-on-month rate was slightly stronger than expected and core CPI was unchanged at 4.0% y/y.

The figures highlight the possible challenges that central banks face in overcoming the final hurdle in reducing inflation all the way down to 2.0%.

Fed rate cut expectations fell back only marginally after the data, suggesting that markets remain overwhelmingly convinced that a rate cut will arrive by May at the latest.

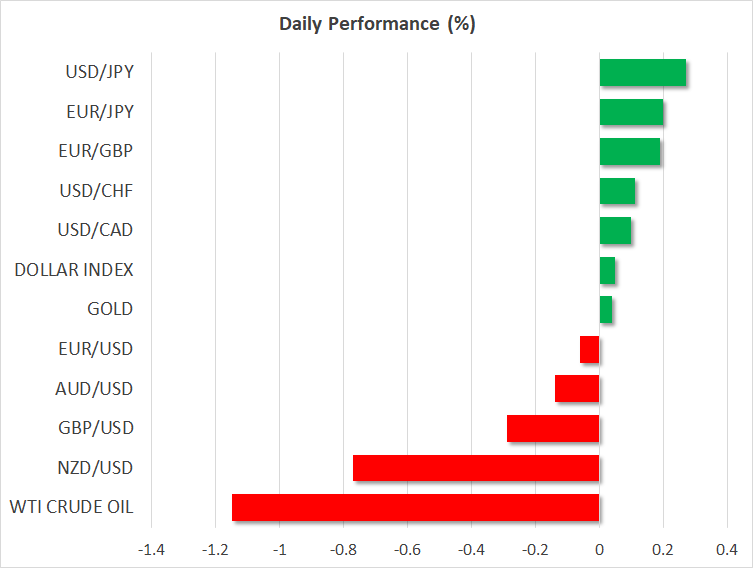

Dollar recovers from post-CPI lows, pound slips on weak data

The US dollar was somewhat firmer on Wednesday as the immediate reaction to the CPI numbers faded, with some investors questioning the sooner rather than later call for rate cuts even as Treasury yields edged slightly lower.

The euro was back below $1.08, while the yen weakened to around 145.80 to the dollar. The pound was one of the worst performers, coming under pressure for a second day on the back of a string of disappointing data.

Yesterday’s soft employment numbers were good news for the Bank of England, which wants to see lower wage growth, but today’s worse-than-expected GDP estimates are somewhat more worrying as it highlights the risk of the UK economy entering a recession.

Britain’s GDP shrank by 0.3% m/m in October, as the services sector contracted and manufacturing output slumped. However, the Bank of England is unlikely to drop its tightening bias when it meets tomorrow, in what would be a mixed blessing for sterling.

Wall Street extends gains despite rate cut and China doubts

But there were few signs of recession worries in equity markets as the rate cut bets continue to support risk assets. The S&P 500 closed at its highest level in almost two years on Wednesday, while the Nasdaq Composite touched the highest since April 2022.

While much of the gains are still being driven by big tech stocks, particularly the Magnificent Seven, there are substantial downside risks heading into today’s FOMC’s decision, and perhaps even more so from Powell’s press conference. The Fed chief will probably attempt to push back on rate cut expectations and leave the hike option firmly on the table. However, it’s also unlikely that Powell will sound too hawkish so investors may yet again brush off any fresh higher for longer warnings.

European shares were trading higher on Wednesday and Asian shares were mostly positive too, with Chinese and Hong Kong indices once again underperforming as investors continue to fret about the lack of any major stimulus announcements by Beijing. The worries come after data over the weekend showed China fell deeper into deflation in November.

.jpg "Fed awaited as stocks jump, dollar slips after US CPI")

Gold stabilised at $4,000, but the upward trend has already broken down

The dollar risks losing support from tariff revenues

The dollar risks losing support from tariff revenues

ZEC as the omen of a brewing storm in crypto

ZEC as the omen of a brewing storm in crypto

Risk markets struggle on lack of bullish catalysts

Supreme Court's Tariff Battle: A Turning Point or More Uncertainty for Global Trade?