Dollar and equities rebound from NFP-led losses as focus turns to US CPI

Signs of optimism after NFP bloodbath

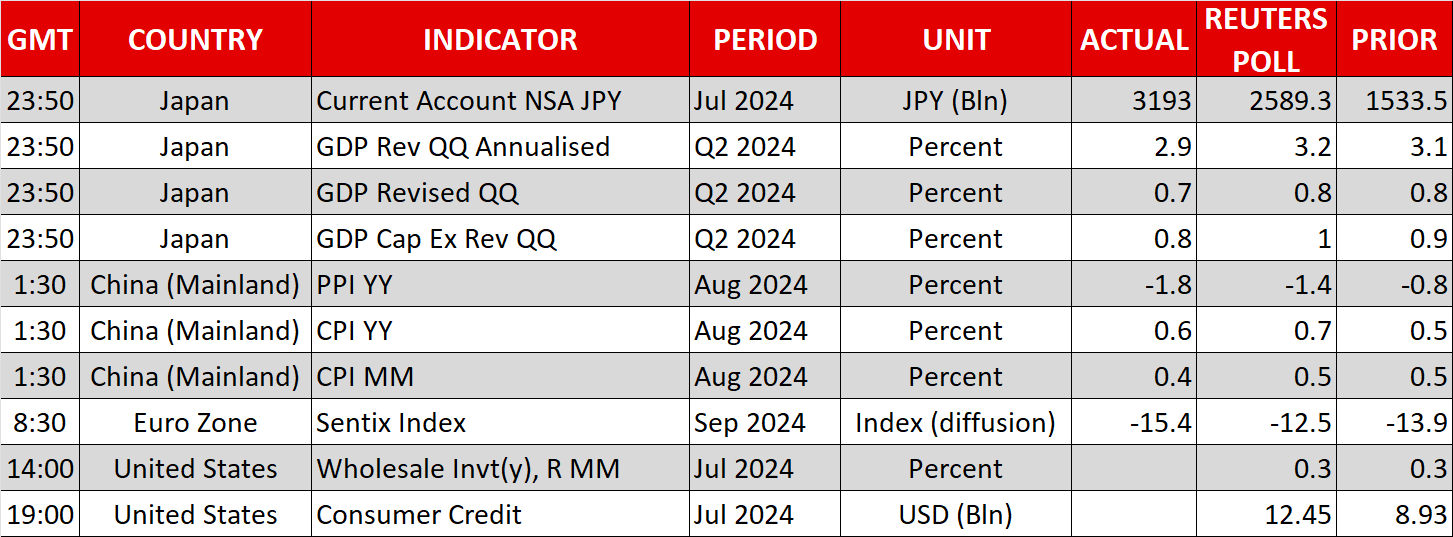

Markets began the second week of September in a somewhat more upbeat mood as US slowdown jitters were put on hold even as inflation data out of China pointed to persistently weak demand in the world’s second-largest economy. Wall Street ended the week with heavy losses, led by a 5.9% drop in the Nasdaq 100, amid growing fears that the Fed has left it too late to take its foot off the brake and concerns about overspending on AI by the Big Tech.

Hopes that Friday’s jobs report would have lifted spirits by bolstering expectations of a 50-basis-points cut by the Fed when it meets on September 17-18 didn’t materialize. Instead, it worsened the uncertainty.

The US labour market added 142k jobs in August, missing expectations of a 160k increase and underscoring concerns that hiring could be grinding to a halt. Yet, the unemployment rate fell slightly to 4.2% while wage growth accelerated somewhat more than expected, giving the Fed little reason to kick off its easing cycle with a double cut.

Waller fails to soothe investor anxiety

Fed officials have not shut the door to a 50-bps reduction in September and even more hawkish members such as Governor Waller are open to the possibility of a larger cut. Speaking on Friday, Waller said he would support front-loading rate cuts “if that is appropriate”.

Other Fed policymakers that were on the wires on Friday also gave their backing to a September cut. However, considering the scale of angst in the markets, it seems that the comments didn’t go far enough in making the case for a 50-bps move, and with no more Fed speak until FOMC day, the sense of disappointment took over, pushing Wall Street lower.

Spotlight on US CPI as Fed blackout begins

Historically, September isn’t the best month for the stock market so the ‘September effect’ could also be at play, exacerbating the selloff. But hope is not lost as there is still the CPI report to go before the Fed meeting and that might explain why equities are rebounding today. The latest inflation numbers due on Wednesday are expected to show another drop in the headline CPI rate in August.

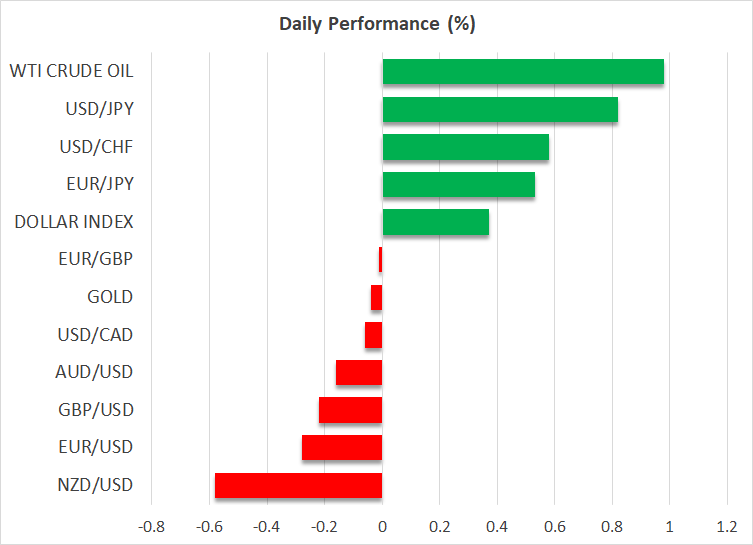

US futures are currently heading higher and European shares are positive too. Asian stocks, however, extended their losses, amid worries about China’s economy following the softer-than-expected CPI and PPI figures.

US dollar and oil pare losses as euro slips ahead of ECB

The pessimism about China weighed on the risk-sensitive Australian and New Zealand dollars, as well as on some commodities such as iron ore. But oil futures bounced back by more than 1%, finding some comfort in the decision by OPEC+ last week to delay the previously announced output increase in October by two months amid a slump in prices lately. Today’s jump could be just a technical recovery after hitting one-year lows on Friday, but it could also be the same realisation as in equity and bond markets that the doom and gloom is probably overdone.

The US 10-year yield is up sharply on Monday, putting the US dollar on a firmer footing after a seesaw session on Friday. The greenback came close to breaching the August low against the yen, but it is back above 143 yen today, while the euro is back in the $1.1050 region after a failed attempt to reclaim the $1.1100 handle last week. Further weakness in the single currency is likely in the coming days as the ECB is expected to cut interest rates on Thursday for a second time this cycle.

.jpg "Dollar and equities rebound from NFP-led losses as focus turns to US CPI")

Investors cheer potential end to US government shutdown

The dollar plays on bets

Is the Gold Bull Done Charging? Year End Checkpoint

Gold Climbs to Two-Week High

Good news for Crypto bargain hunters

Good news for Crypto bargain hunters

EBC Markets Briefing | Yen lower on weak data; market frowns at Musk's pay package