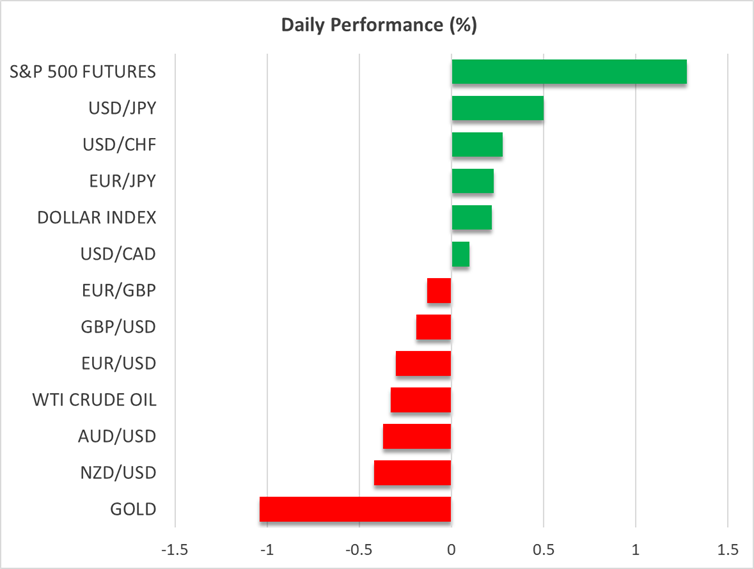

Dollar benefits amidst a muted risk-on reaction

US and UK markets reopen

Market participants are back in action following the US and UK bank holidays, which resulted in extremely low trading volumes during Monday’s session. A muted risk-on reaction is present in markets, with the US dollar recording some gains against peripheral currencies and European equities feeling frisky.

The prevailing issues remain unresolved, with trade deals, or the lack thereof, generating a number of headlines even during yesterday's quieter session. Despite repeated commentary, there have been no announcements since the preliminary US-China trade agreement on May 12, which reduced tariffs for 90 days.

A US-India trade deal is almost ready

US-India negotiations appear to be progressing well, and this will probably be the next trade deal to be agreed and announced by US President Trump. The same cannot be said for Japan and the EU, though. US-Japan discussions have reached a temporary deadlock, as the Japanese side continues to seek zero tariffs, with Trump appearing unwilling to grant special status to America’s closest Asian ally.

Similarly, following last Friday’s shenanigans, there seems to be a renewed push for an agreement between the US and the EU. However, the critical issues are yet to be tackled, thus making the waiting period until the July 9 deadline rather tumultuous.

Treasury yields ease somewhat

Meanwhile, US Treasury yields have retreated a few basis points overnight, with the 10-year yield dropping below 4.5% once again. The current “game of debt” has clear losers, with both the US and Japan feeling the brunt of the pressure as bond vigilantes potentially test the reaction from their respective central banks. The BoJ already owns more than half of the Japanese government bond market, thus making it riskier and more difficult to affect yields. On the other hand, the Fed is in a much better position to intervene if there is a need down the line.

More importantly, these yield movements are ‘messing’ with the monetary policy stance of both the Fed and the BoJ. The tightening in financial conditions is acting as a rate hike, which is a positive development in Japan’s case as the BoJ remains on a tightening path. However, their effect is the opposite for the Fed, which is still on an easing path.

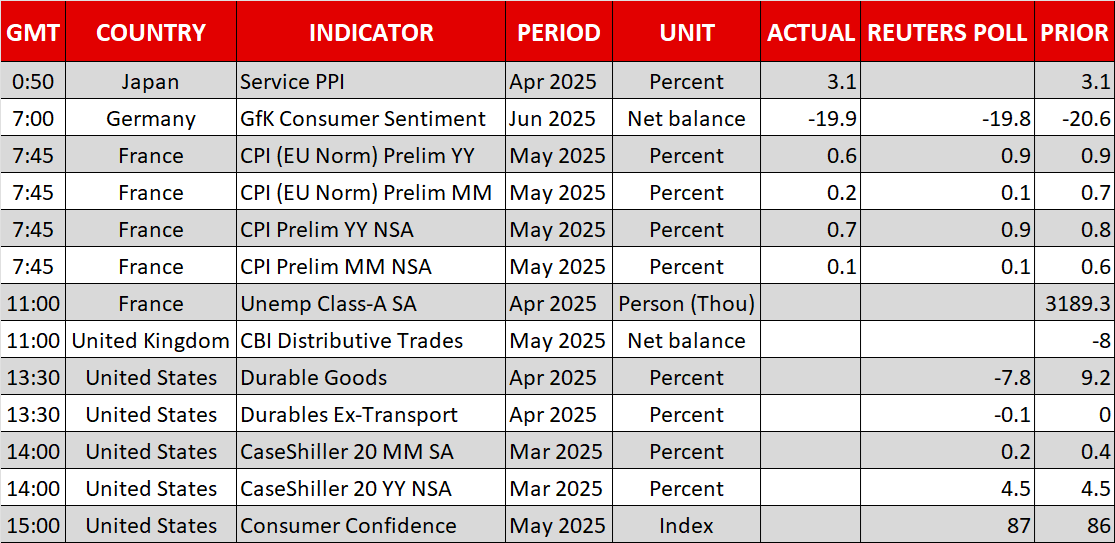

Busy calendar today

Starting today, US economic releases will be in the spotlight, with Fed doves hoping for a soft set of data prints to support their behind-the-door arguments for a rate cut sooner rather than later, especially now that financial conditions have tightened.

Durable goods orders and house price data will be released today, although the market’s focus will mostly be on the May Consumer Confidence survey. In the April report, the headline figure dropped to levels not seen since the Covid period, while the expectations index tanked to the lowest level since October 2011. A failure from both indicators to record a sizeable recovery today might signal significant damage to consumers’ spending appetite from Trump’s tariff shenanigans.

Similarly, US note auctions are on the menu this week, with today’s 2-year offering expected to go smoothly. However, the real test of market appetite for US debt will be the 7-year auction on Thursday, an area of the curve that is not traditionally popular with bond investors.

Gold ignores headlines about another failed ceasefire agreement in Gaza

Finally, Israel appears to have rejected a US-led ceasefire proposal that Hamas has agreed to, which would include the release of 10 hostages in exchange for a 70-day truce. Interestingly, gold is ignoring the latest development, dropping towards the $3,300 area after trading above the $3,360 level for the first time in over a month.

.jpg "Dollar benefits amidst a muted risk-on reaction")

Why a Strong Swiss Franc Is Hurting Switzerland’s Economy—and What the Central Bank Might Do About It

Why a Strong Swiss Franc Is Hurting Switzerland’s Economy—and What the Central Bank Might Do About It

Why Oil prices might be a rollercoaster ride this summer

US data hurt the dollar, ECB to cut rates again

EUR/USD eyes key resistance as ECB decision looms

Gold poised for further gains as US economic outlook deteriorates

Silver Shines, Dollar Wavers | 5th June, 2025